Financial stability is dependent on the smooth flow of money. Most people use a bank account as a central point of life. Salaries arrive there. Expenses such as rent, utilities, and groceries go out from it. At times, this flow is abruptly stopped, which is why banks freeze accounts. This may be done by the bank or by a legal authority. It prevents you from having access to your money. The account stays open and may still receive deposits. However, you will not be able to withdraw cash, send transfers, or pay bills. Modern banks use strict rules and automated fraud checks, and many times these systems cause freezes. Understanding why banks freeze accounts helps you take control of your finances again.

What Is a Bank Account Freeze?

At its core, a bank account freeze is a suspension of all outgoing transactions. Think of it as a digital barrier that allows money to enter but prevents it from leaving. To better understand your account activity and track any unusual transactions that might trigger a freeze, check out our guide on How to Read a Bank Statement (Beginner Guide) You cannot swipe your debit card, use an ATM, or even move money between your own checking and savings accounts.

As of 2026, these freezes have become increasingly common due to two primary drivers: sophisticated algorithms hunting for identity theft and legal mandates aimed at debt collection. Whether the freeze is a protective measure by your bank or a punitive one from a creditor, the result is the same—a total loss of immediate liquidity.

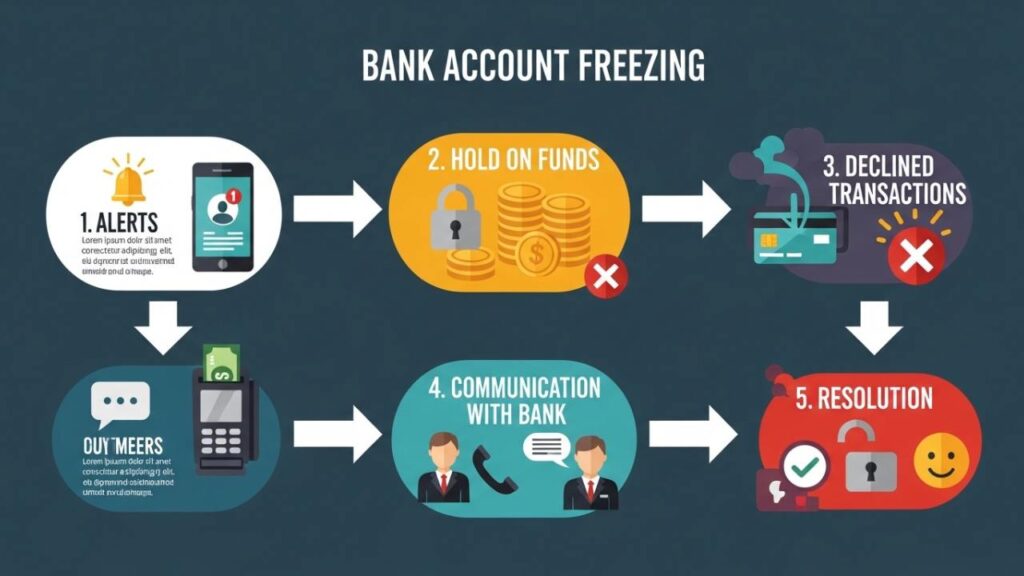

How It Works: The Step-by-Step Process

The transition from a functional account to a frozen one often happens in seconds, following a specific administrative sequence.

- The Trigger: A specific event flags the account for review. This might be a “burst” of high-dollar transactions in an unfamiliar country, or perhaps a court clerk filing a notice of a legal judgment against you.

- Internal Restriction: Once flagged, the bank’s security or legal department places a “hold” on the funds. At this moment, any pending checks or scheduled ACH transfers (like your car insurance or mortgage) will likely be returned as unpaid.

- The “Silent” Phase: In cases involving debt or suspected money laundering, banks are often legally discouraged or even barred from notifying you in advance. This prevents individuals from emptying the account before the freeze is finalized.

- Communication and Verification: Once you discover the freeze—usually by having a card declined—you must contact the bank to identify the department responsible. You might need to verify your identity or provide proof of the source of your funds.

- Resolution and Release: The freeze is lifted only when the underlying issue is resolved. This could mean proving a transaction was legitimate, paying off a debt, or waiting for a government agency to send a release notice to the bank.

Key Features and Core Components

A bank freeze isn’t a singular event; it is the result of several interacting technical and legal layers.

Algorithmic Surveillance

Modern banking relies on “Behavioral Analytics.” These systems build a profile of your spending habits. If you suddenly deviate from these patterns—such as making three large transfers to a new digital wallet—the AI may freeze the account automatically to mitigate potential theft.

Legal Levies and Writs

If a creditor wins a lawsuit against you, they can obtain a “Writ of Execution.” This document compels your bank to freeze an amount equal to the debt. The bank is a neutral third party here; they are legally bound to follow the court’s order, regardless of your personal financial needs.

Statutory Requirements (KYC)

“Know Your Customer” (KYC) laws require that banks keep the information of customers updated. Banks have to establish your identity. If your ID expires, the bank may do something. If you fail to respond to requests about updates for taxes, the bank can respond. The bank will have the option to freeze your account. This it does to comply with regulations. The freeze remains until you get your records straight.

Benefits and Advantages of Account Freezes

While a freeze is a major disruption, it plays a vital role in maintaining the security of the broader financial system.

Immediate Fraud Mitigation

The most obvious benefit is the “emergency brake” function. If a hacker gains access to your online banking, a proactive freeze can save your entire life savings. In these instances, the temporary inconvenience of a freeze is far preferable to the permanent loss of capital.

Asset Preservation

In lawsuits such as a divorce or splitting up an estate, courts can order that bank accounts be frozen. This action prevents people from hiding or spending money. It protects the assets until a judge makes a decision. The court then determines how to divide the funds. This process ensures all parties remain fair and equal.

Systemic Integrity

By halting suspicious or high-risk transfers, banks help curb illegal activities like money laundering. This oversight keeps the domestic banking system compliant with international standards, which ultimately protects the value and stability of the currency.

Risks, Drawbacks, and Limitations

The secondary effects of a frozen account are often more damaging than the freeze itself.

The Domino Effect of Failed Payments

Frozen accounts can cause failed payments, NSF fees, and service cancellations. If you’re managing multiple debts that could lead to a bank freeze, learning How Debt Consolidation Works (And When It’s a Bad Idea) can help you evaluate safer strategies.

Lengthy Resolution Windows

Banks are quick to freeze but often slow to thaw. Even after you provide the requested documentation, it can take days for a human representative to review the file and manually lift the restriction. If the freeze involves a government agency, the wait time can stretch into weeks.

Challenges with Exempt Funds

Social Security and disability payments are generally “judgment proof,” meaning creditors cannot take them. However, banks sometimes freeze the entire balance first and put the burden on the consumer to prove which funds are exempt. This creates a period where an individual may have no money for food or medicine while waiting for a legal review.

Who It May Be Suitable For

While usually involuntary, there are times when a freeze is a useful tool for the consumer.

- Security-Conscious Users: If you lose your wallet or notice a strange login attempt, you should immediately request a voluntary freeze on your accounts.

- Fiduciaries: Those acting as a “Power of Attorney” for an elderly relative may use freezes to prevent the relative from falling victim to phone scams or predatory solicitations.

- Estate Administrators: Banks freeze the account of a deceased person as a normal process. This action conserves the funds. This ensures that the estate will pay off its debts first. After that, the rest of the money is distributed among the heirs.

Who Should Be Cautious

Certain behaviors or financial situations increase the likelihood of an unexpected freeze.

- Frequent International Travelers: Using your card in multiple countries within a short window can look like fraudulent activity to an automated system.

- Users of Personal Accounts for Business: If you run a high-volume business through a standard personal checking account, the bank may freeze it for “improper account usage” or suspected tax evasion.

- Those with Outstanding Judgments: If you have a history of unpaid medical debt or defaulted loans, you are statistically more likely to face a sudden legal levy.

Alternatives and Related Options

Relying on a single bank account is a significant risk in the digital age. Consider these alternatives to ensure you are never completely cut off from your money.

Geographic and Institutional Diversification

Opening a second account at a completely different bank—preferably one that is not linked to your primary loans—provides a safety net. For more tips on choosing and managing bank accounts to protect your money, see the CFPB guide on bank accounts. If Bank A freezes your account due to a glitch, you can still use Bank B to cover your immediate bills.

Keeping “Cash on Hand”

Carry some cash or get a pre-paid card that is not connected to your bank. This provides a 48-hour buffer in times of emergency.

Credit Card Utilization

Using a credit card for daily expenses, and paying it off from your checking account, adds a layer of protection. If the checking account is frozen, your “buying power” remains intact on the credit card for a period of time, giving you room to resolve the issue.

Frequently Asked Questions

1. Can my bank freeze my account because of my spouse’s debt?

If you have a joint account, the answer is generally yes. Creditors can often freeze the entire balance of a joint account to satisfy the debt of just one owner, regardless of who deposited the money.

2. Will I still earn interest on a frozen account?

Typically, yes. Because the account is still open and the funds are still held by the bank, interest-bearing accounts should continue to accrue interest at the standard rate during the freeze.

3. What is the difference between a “frozen” account and a “blocked” account?

The terms are often used interchangeably, but a “block” usually refers to a specific merchant or transaction type being stopped, while a “freeze” is a total suspension of all outgoing activity.

4. Can the bank take my money while it is frozen?

A freeze is the first step. If the freeze is due to a legal judgment, the bank will eventually be required to “remit” (send) the funds to the creditor or the court after a certain waiting period, unless you successfully contest the levy.

Conclusion

A frozen bank account is a significant hurdle that can disrupt every aspect of your financial life. Whether triggered by an overzealous fraud algorithm or a legitimate legal debt, the result is a loss of the autonomy we usually take for granted. By maintaining a professional relationship with your bank, keeping your contact information current, and diversifying where you hold your capital, you can minimize the impact of these administrative actions. While you cannot always prevent a freeze, being prepared with secondary payment methods and a clear understanding of the resolution process is the best way to maintain your financial resilience.