Financial clarity begins with knowing exactly where your money goes. While mobile banking apps offer a convenient, real-time glimpse at your balance, the formal bank statement remains the definitive legal record of your financial life. Developing the habit of reviewing this document is a cornerstone of personal finance; it allows you to audit your spending, verify that deposits have cleared, and identify unauthorized activity before it compromises your security. If you want to understand how read bank statement, it’s important to recognize that this document is more than a simple list of numbers; it is a vital tool for reconciliation.

By examining these records monthly, you can uncover forgotten subscriptions, catch administrative errors, and spot avoidable fees. This guide breaks down the anatomy of a statement, providing a structured approach to interpreting the data and explaining what to do if the numbers don’t add up.

What Is a Bank Statement?

At its core, a bank statement is a formal summary of all financial activity within a specific window of time, usually 30 days. Issued by your financial institution, these documents are available either as physical mail or as digital PDFs (e-statements) via your online portal.

The statement serves as the “official word” on your account. It captures your starting balance, every incoming credit, every outgoing debit, and the final tally at the end of the cycle. Because of its status as a verified legal document, you will often need these statements when proving your financial standing for a lease, a mortgage, or a loan application.

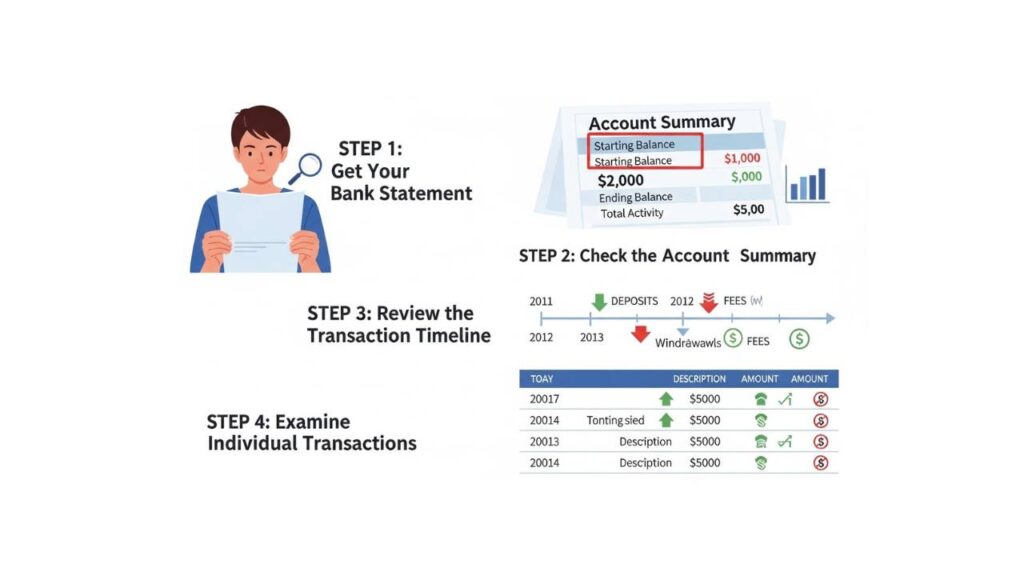

How It Works: A Step-by-Step Review

Navigating a page full of transactions can feel tedious, but the process becomes intuitive when you follow a consistent sequence.

- Validate the Basics: Confirm that the name and address in the header are current. Check the account number to ensure you are looking at the correct checking or savings file.

- Define the Timeline: Identify the “Statement Period.” It is a common misconception that statements follow the calendar month; many cycles begin mid-month (e.g., March 12 to April 11).

- Review the Big Picture: Look at the Account Summary box. Does the “Beginning Balance” match the “Ending Balance” from last month? If not, there may be an unresolved discrepancy.

- Audit Individual Transactions: Go through the line items chronologically. Verify that every withdrawal matches your actual purchases and that every deposit you made is fully accounted for. For additional tips on monitoring your account, avoiding errors, and protecting yourself from unauthorized transactions, the Consumer Financial Protection Bureau (CFPB) offers practical guidance that is easy to follow and reliable.

- Check the “Fine Print”: Look for a specific section detailing interest earned or service fees. This reveals the “hidden” costs of the account and the small gains from any interest-bearing features.

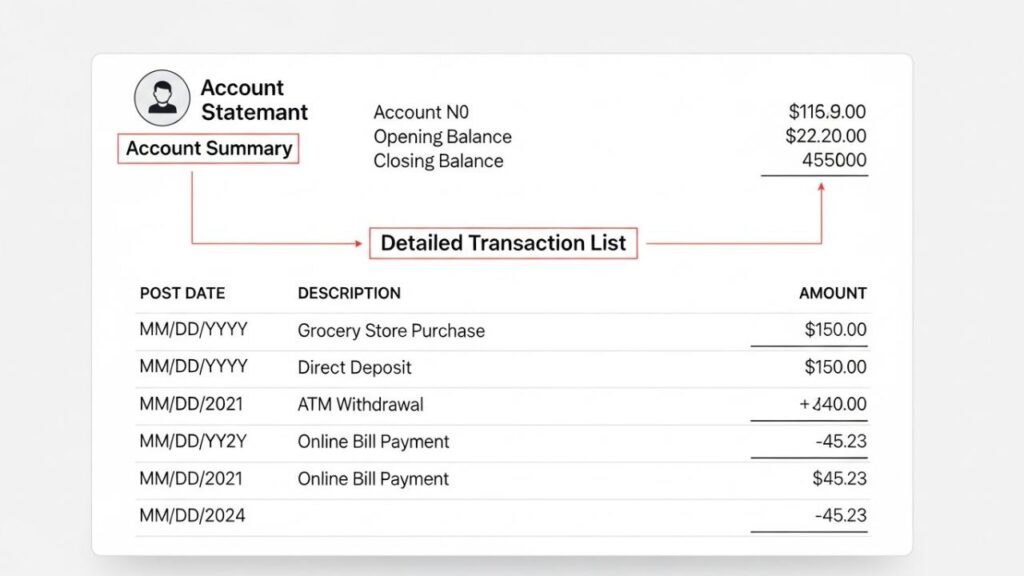

Key Features and Core Components

While every bank has a proprietary design, they all rely on several standardized sections to convey information.

The Account Summary

Usually found on the first page, this high-level overview aggregates your activity into a few key numbers: total deposits, total withdrawals, and any fees charged. It acts as a quick “health check” for your monthly cash flow.

Detailed Transaction List

This is the heart of the document. Each entry typically displays:

- Post Date: When the bank finalized the transaction.

- Description: The merchant’s name or a system-generated code.

- Amount: Credits (money in) and Debits (money out) are usually placed in separate columns or distinguished by plus and minus signs.

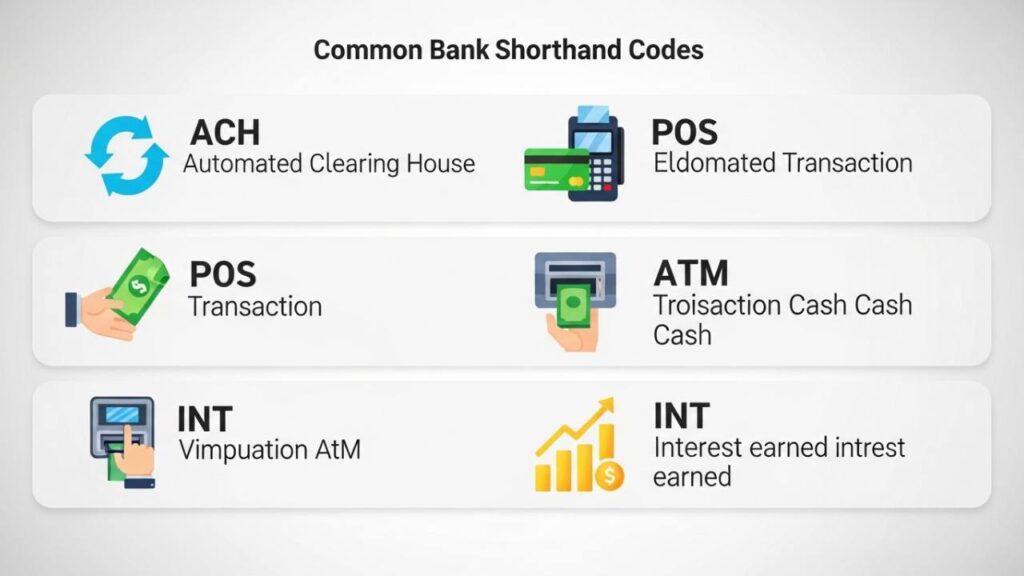

Standardized Shorthand

Banks use specific codes to categorize movement. You will likely see:

ACH: Electronic transfers, such as your direct-deposited salary.

POS: A “Point of Sale” transaction made with your debit card.

ATM: Any cash-related activity at a teller machine.

INT: The interest the bank paid you during that cycle. Some bank statements may also include unfamiliar abbreviations or transaction labels. If you notice terms you do not recognize, read What Is ADTQ in a Bank Account? to understand how banks use internal processing codes and account terminology.

Benefits and Advantages

Consistently reading your statement offers more than just peace of mind; it provides tangible financial protection. Accuracy is the primary benefit. Even the most advanced banking systems can occasionally double-process a charge or fail to post a credit correctly. Manual verification is your best defense against these rare but costly glitches.

Furthermore, it encourages behavioral awareness. A consolidated list of every minor purchase—like daily coffee or streaming services—can be more impactful than seeing individual app notifications. Finally, it serves as a crucial security layer. Most institutions require you to report errors within 60 days to qualify for full consumer protection. Regularly checking your statement ensures you never miss that deadline.

Risks, Drawbacks, and Limitations

Despite their utility, bank statements are not perfect tools and come with specific caveats:

- Historical Lag: A statement is a “look back” at the past. It does not account for “pending” transactions—purchases you made today that haven’t cleared yet. Consequently, your statement balance may appear higher than the actual funds you have available to spend.

- Cryptic Descriptions: Merchant names are often confusing. A local boutique might appear on your statement as a vague corporate holding company, making it difficult to remember if the charge was legitimate.

- Privacy Concerns: Physical statements are a primary target for identity thieves. If you receive paper records, they must be stored securely or shredded; leaving them in an unsecured mailbox presents a significant risk.

- Hidden Liabilities: Statements only show what has cleared. If you wrote a check three weeks ago that hasn’t been cashed, that money is still in your account according to the statement, but it is technically spoken for. Misreading your available balance can sometimes result in overdrafts or declined transactions. To understand the consequences, see What Happens If You Have Insufficient Funds in Your Bank Account?

Who It May Be Suitable For

Regularly reviewing a statement is a universal best practice, but it is especially vital for:

- Budget-Conscious Individuals: Those who want to categorize their spending to stay within financial goals.

- Self-Employed Workers: People who must track deductible business expenses separately for tax season.

- Future Homebuyers: Individuals preparing for the “underwriting” process, where lenders will scrutinize every deposit and withdrawal.

Who Should Be Cautious or Avoid It

While no one should avoid their statements entirely, some should be wary of relying only on the monthly document:

- Joint Account Users: If two people share an account, a monthly review might lead to confusion if they aren’t communicating about their daily spending.

- Active Fraud Victims: If your account has been compromised recently, waiting 30 days for a statement is too long; you should utilize real-time alerts instead.

Alternatives and Related Options

If a once-a-month summary feels too infrequent, consider these modern alternatives:

- Digital Banking Apps: Most banks allow you to scroll through your history 24/7, including “pending” items.

- Transaction Alerts: You can often set up text or email notifications for any transaction over a certain dollar amount.

- Aggregator Tools: Services that link multiple bank accounts into one dashboard can provide a broader view of your net worth, though the data still originates from your bank statements.

Frequently Asked Questions

1. What if the merchant name on my statement looks unfamiliar?

Don’t panic immediately. Search the name online or look at the transaction date and amount to see if they match a receipt you have. Many stores use “doing business as” (DBA) names that differ from their storefront signs.

2. Is there a difference between my statement balance and my available balance?

Yes. Your statement balance is a fixed snapshot from the end of the period. Your “available balance” is what you have right now, after accounting for recent spending and any “holds” the bank has placed on your funds.

3. How should I dispose of old statements?

Because statements contain sensitive account data, you should never throw them in the regular trash. Use a cross-cut shredder or a professional document destruction service to protect yourself from identity theft.

4. Can I use a digital statement for a mortgage application?

In almost all cases, yes. Lenders accept downloaded PDF e-statements as long as they are complete and show all pages, including the ones that are intentionally left blank.

Conclusion

The bank statement remains one of the most reliable records in the financial world. By taking fifteen minutes each month to verify the header, summarize your activity, and audit individual line items, you protect yourself from errors and fraud. While technology offers many ways to track money in real-time, the formal statement provides the high-level perspective necessary for long-term financial health. It is a simple habit that ensures you remain the primary authority over your own money.