Asset allocation is the foundational process of dividing an investment portfolio among different asset categories, such as stocks, bonds, and cash. The primary objective of this strategy is to balance risk and reward by apportioning a portfolio’s assets according to an individual’s goals, risk tolerance, and investment horizon. It matters because different classes often perform differently under various market conditions; when one category loses value, another may stay stable or increase. This diversification is designed to protect the investor from significant losses while allowing for steady, long-term growth.

What Is Asset Allocation?

At its core, taking an asset approach means evaluating, dividing, or managing individual items of value one at a time, rather than looking at them as a single combined “pool” or total sum. In the context of a beginner’s investment strategy, allocation is the roadmap for how you distribute your capital.

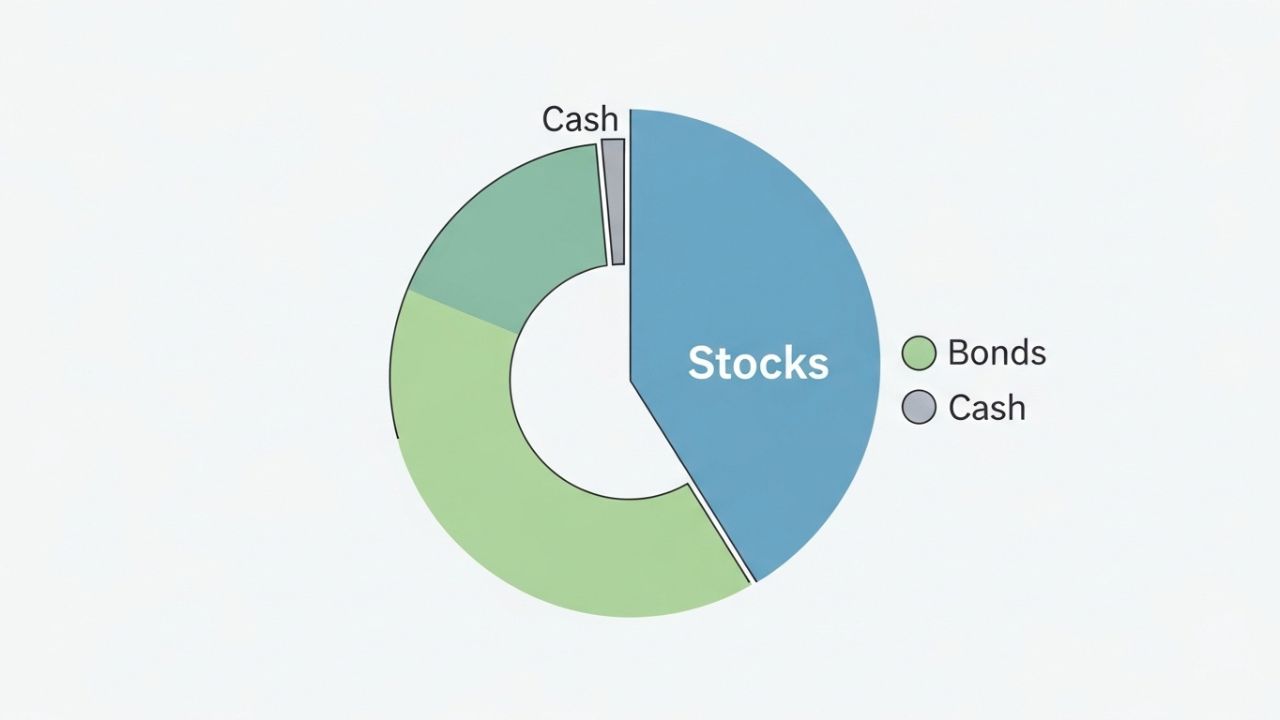

It involves identifying specific “buckets” of investments—such as equities (stocks), fixed income (bonds), and cash equivalents—and determining what percentage of your total money should live in each bucket. By viewing your financial profile through this lens, you move away from emotional decision-making and toward a disciplined framework. This method ensures that you are not over-exposed to a single type of economic risk.

How It Works

Implementing an asset allocation strategy typically follows a structured, step-by-step process to ensure the portfolio aligns with the investor’s specific needs.

- Define Your Time Horizon: Determine when you will need to access the money. A longer time horizon (20+ years) typically allows for a higher exposure to volatile assets, whereas a short horizon (1–3 years) requires stability.

- Assess Risk Tolerance: This is an honest evaluation of how much market volatility you can withstand without selling in a panic. It is the balance between the desire for returns and the ability to stomach losses.

- Select Asset Classes: Choose which categories to include. Common choices include domestic stocks, international stocks, government bonds, corporate bonds, and money market funds. Some investors also diversify beyond stocks and bonds by adding alternative assets to their portfolios. Pros and Cons of Investing in Gold for Long-Term Wealth explores whether gold can help improve stability during periods of inflation or market uncertainty.

- Determine Percentage Weights: Assign a percentage to each category (e.g., 60% stocks, 40% bonds). This creates your “target allocation.”

- Execute the Purchases: Buy the individual securities or funds that satisfy the determined percentages.

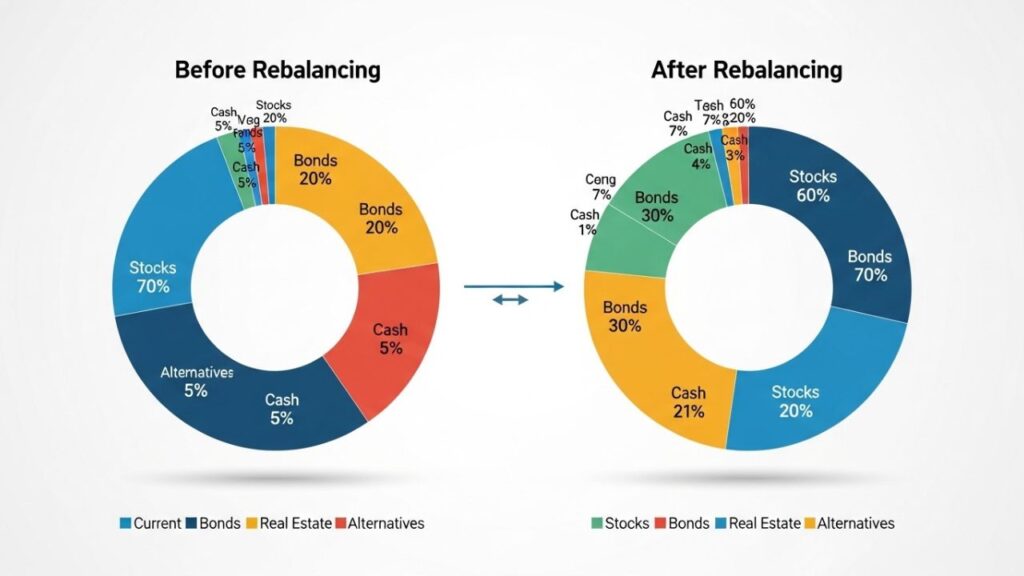

- Periodic Rebalancing: Over time, some assets will grow faster than others, changing your percentages. Rebalancing involves selling some of the “winners” and buying more of the “underperformers” to return to your original target.

Key Features or Core Components

The effectiveness of asset allocation relies on several fundamental components that work together to stabilize a portfolio.

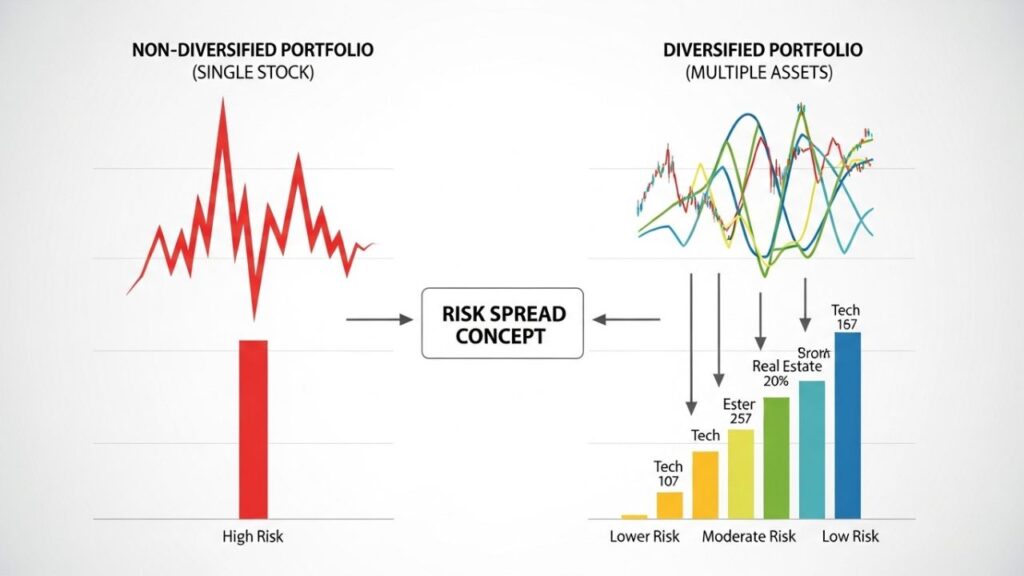

Diversification

This is the practice of spreading investments within and across asset classes. While allocation decides the “buckets,” diversification ensures that within the “stock bucket,” you aren’t just holding one company. Investors seeking broad international diversification may also benefit from learning about What Is a Global Equity Fund? Beginner Guide, which explains how global funds spread investments across multiple countries and markets.

Correlation

Correlation measures how different assets move in relation to one another. A key feature of a well-allocated portfolio is holding assets with “low correlation,” meaning they do not all move in the same direction at the same time.

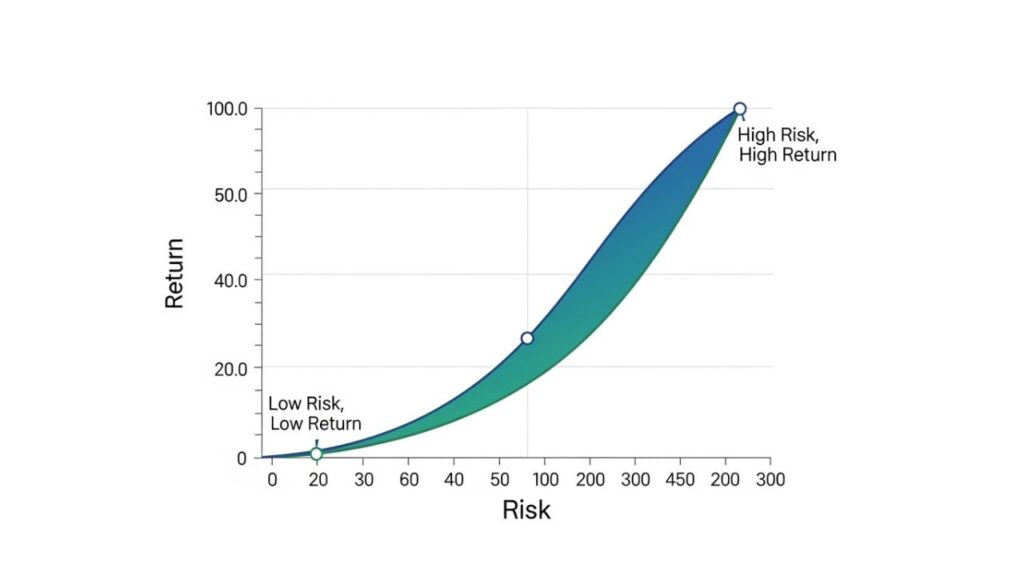

Risk-Return Tradeoff

This is the principle that potential return rises with an increase in risk. Stocks offer higher potential returns but come with higher risk, while bonds offer lower returns with generally lower risk. Asset allocation manages this tradeoff.

Benefits or Advantages

A disciplined approach to asset allocation offers several realistic advantages for the long-term investor.

- Risk Mitigation: By spreading investments across different sectors, the impact of a decline in any single asset class is softened by the performance of others.

- Emotional Discipline: Having a pre-set plan helps investors avoid the temptation to chase “hot” stocks or sell during a market downturn, as the allocation dictates the strategy rather than headlines.

- Customization: Asset allocation is not “one size fits all.” It can be tailored specifically to whether an investor is a 22-year-old starting their first job or a 65-year-old entering retirement.

- Simplified Decision Making: Once the target allocation is set, the investor no longer needs to wonder “what should I buy today?” The plan provides the answer.

Risks, Drawbacks, or Limitations

While asset allocation is a widely accepted strategy, it is not a guarantee against loss and has its own set of limitations.

- No Protection Against Systemic Risk: In a major global financial crisis, correlations can “break.” This means that almost all asset classes might lose value simultaneously, rendering the allocation less effective in the short term.

- Lower Potential for “Home Runs”: Because you are diversified, you will never have 100% of your money in the single best-performing stock of the year. You trade the chance of massive gains for the security of stability.

- Inflation Risk: If an allocation is too conservative (e.g., 100% cash or low-interest bonds), the portfolio may not grow fast enough to keep up with the rising cost of living, leading to a loss of purchasing power over time.

- Complexity of Rebalancing: For a beginner, the act of selling assets that have performed well to buy those that have performed poorly can be counterintuitive and may trigger tax implications in non-retirement accounts.

Who It May Be Suitable For

Asset allocation is suitable for almost any investor who seeks a methodical, long-term approach to wealth building. It is particularly effective for:

- Retirement Savers: Those who have a specific end date in mind and need to manage risk as they approach that date.

- Passive Investors: Individuals who do not have the time or interest to research individual companies daily and prefer a “set and monitor” approach.

- Beginners: Those who want a clear framework to start investing without feeling overwhelmed by the thousands of individual stock options available.

Who Should Be Cautious or Avoid It

While most benefit from this strategy, it may not be the primary focus for certain individuals:

- Speculators: Those looking for short-term, high-risk gambles or “get-rich-quick” opportunities will find the slow, steady nature of asset allocation frustrating.

- Day Traders: Individuals focused on technical analysis and minute-by-minute price movements generally operate outside the bounds of long-term asset allocation.

- High-Debt Individuals: Those with high-interest debt (like credit cards) should generally prioritize debt repayment over establishing a complex asset allocation, as the interest saved is a guaranteed “return.”

Alternatives or Related Options

If a manual asset-by-asset allocation seems too complex, there are several related options:

- Target-Date Funds: These are mutual funds that automatically adjust their asset allocation over time based on a specific retirement year.

- Index Fund Investing: This involves buying a single fund that tracks an entire market index (like the S&P 500), which inherently provides a level of equity diversification.

- Robo-Advisors: These are automated platforms that use algorithms to build and rebalance a portfolio for you based on a risk questionnaire.

Frequently Asked Questions

1. How often should I rebalance my asset allocation?

Most experts suggest reviewing your allocation once or twice a year, or whenever an asset class moves more than 5% away from its original target weight.

2. Does asset allocation prevent all losses?

No. Asset allocation is a risk management tool, not an insurance policy. As explained by Investor.gov’s educational overview of asset allocation, diversification and allocation strategies may help manage portfolio risk, but they cannot eliminate losses caused by market volatility.

3. Should I change my allocation when the market is doing poorly?

Generally, no. Changing your strategy during a downturn is often a reaction to fear. A well-designed allocation should already account for the fact that markets will occasionally decline.

4. What is the “Rule of 100” in asset allocation?

This is an old rule of thumb suggesting you subtract your age from 100 to determine the percentage of stocks you should hold. For example, a 30-year-old would hold 70% stocks. Many modern advisors now use 110 or 120 as the base number to account for longer life expectancies.

Conclusion

Asset allocation is a fundamental principle of sound financial management. By evaluating investments on an asset-by-asset basis and organizing them into a coherent structure, investors can manage risk more effectively and maintain a clear path toward their goals. It requires a balance of stocks for growth, bonds for income and stability, and cash for liquidity. While it does not eliminate the inherent risks of the financial markets, it provides a disciplined framework that helps beginners navigate the complexities of investing with confidence and clarity.