For many homeowners, the value built up in a property represents their most significant financial reservoir. Home equity—the gap between what your home is worth on the open market and what you still owe your lender—grows quietly as you make mortgage payments and as local real estate values climb. This accumulated wealth can be a powerful tool, offering a way to access large sums of capital at interest rates that are typically much lower than those of credit cards or personal loans.

However, tapping into this asset is not a decision to be made lightly. The two primary methods for doing so—the Home Equity Loan and the Home Equity Line of Credit (HELOC)—serve different purposes and carry distinct structures. While both use your residence as collateral, they impact your monthly cash flow and long-term financial health in very different ways. This guide explores the mechanics, benefits, and inherent risks of these two financial products to help you understand which might better align with your specific goals.

What Are Home Equity Loans and HELOCs?

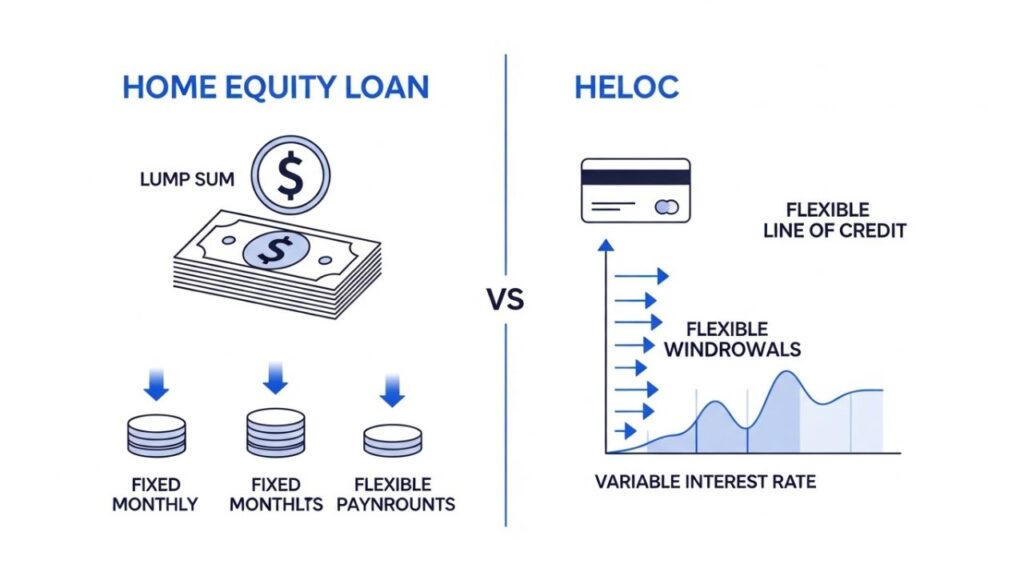

At its simplest, a Home Equity Loan functions as a second mortgage. You receive a one-time payment of cash upfront and repay it over a set period, usually with a fixed interest rate. Because the terms are locked in at the start, you know exactly what your monthly payment will be from the first day until the debt is fully retired. This predictability makes it a staple for those who need a specific amount of money for a singular purpose.

Conversely, a Home Equity Line of Credit (HELOC) operates more like a credit card that is secured by your home. Instead of a lump sum, the lender grants you a maximum credit limit. You can withdraw as much or as little as you need during a specific timeframe, paying interest only on the amount you actually use. Because HELOCs generally feature variable interest rates, the cost of borrowing can shift alongside broader market trends, offering more flexibility but less certainty than a standard loan.

How These Products Work

Navigating the application and funding process involves several standardized steps. Lenders follow a rigorous path to ensure that both the borrower and the collateral meet specific safety margins.

- Establishing Current Value: The process begins with a professional appraisal. A lender needs a documented, objective valuation of your property to determine how much “room” there is to borrow.

- Determining Borrowing Power: Lenders use the Loan-to-Value (LTV) ratio to set limits. For example, if a bank allows an 80% LTV, your total debt (primary mortgage plus the new equity product) cannot exceed 80% of the home’s appraised value.

- Financial Underwriting: Beyond the home itself, the lender examines your “borrower profile.” This includes verifying your income, checking your credit score, and ensuring your debt-to-income (DTI) ratio remains within healthy limits.

- The Closing Phase: Similar to a primary mortgage, there is a formal closing. You will review disclosures and pay fees such as origination charges, title searches, and recording fees.

- Accessing the Funds: If you choose a loan, the full balance is deposited into your account shortly after closing. If you choose a HELOC, you receive a set of checks or a linked card to draw funds as the need arises.

Key Features and Core Components

Characteristics of a Home Equity Loan

- Total Disbursement: You get the entire loan amount in one transaction.

- Interest Rate Stability: The rate is fixed, protecting you from future market spikes.

- Standard Amortization: Your payments are calculated so that by the end of the term, the loan is completely paid off.

- Structured Timeline: Terms are usually clear-cut, ranging from 5 to 20 or even 30 years.

Characteristics of a HELOC

- Revolving Access: As you pay back the principal, those funds become available to borrow again.

- Fluctuating Rates: Most HELOCs have variable rates that rise and fall based on an index like the U.S. Prime Rate.

- Payment Flexibility: During the initial draw period, many lenders offer interest-only payment options to keep costs low in the short term.

- Convertibility: Some modern HELOCs allow you to “lock in” a portion of your balance at a fixed rate, though this varies by lender.

Benefits and Advantages

The Security of a Fixed Loan

The primary appeal of a Home Equity Loan lies in its transparency. In an uncertain economy, knowing that your interest rate will never increase provides significant peace of mind. This product is particularly advantageous for debt consolidation. By taking out a fixed-rate loan to pay off high-interest credit cards, a homeowner can trade multiple unpredictable bills for a single, lower-interest payment that has a clear “light at the end of the tunnel.” Homeowners often use this strategy as part of a broader financial restructuring approach, which is explained in detail in How Debt Consolidation Works (And When It’s a Bad Idea).

The Adaptability of a Line of Credit

HELOCs shine in scenarios where expenses are spread out over time. If you are embarking on a major home renovation, costs rarely hit all at once. A HELOC allows you to pay contractors in stages, ensuring you aren’t paying interest on $50,000 when you’ve only spent $10,000 so far. Furthermore, having an open line of credit can serve as a robust financial safety net, providing liquidity for emergencies without the need to take on a permanent monthly loan payment unless the funds are actually utilized.

Risks, Drawbacks, and Limitations

The Risk of Foreclosure

It is vital to remember that these are secured debts. Unlike a medical bill or a personal signature loan, failing to meet the terms of a home equity agreement gives the lender a direct path to take ownership of your property. Using your home as a “piggy bank” fundamentally ties your shelter to your ability to manage debt. If your financial circumstances change—such as through job loss or illness—this debt becomes a direct threat to your housing security.

Hidden Costs and Fees

Borrowing against equity is rarely free. Beyond the interest, homeowners must contend with closing costs that can total thousands of dollars. HELOCs may also carry annual participation fees or “inactivity fees” if you don’t use the line of credit often enough. When you factor in appraisals and legal fees, the “effective” cost of borrowing may be higher than the advertised interest rate suggests.

The “Balloon” Effect in HELOCs

One of the most common pitfalls of a HELOC is the transition from the draw period to the repayment period. Many borrowers grow accustomed to making small, interest-only payments for ten years. When the repayment period hits, the monthly bill suddenly includes the principal, often leading to a “payment shock” that can strain a household budget to the breaking point.

Who It May Be Suitable For

A Home Equity Loan might be the right fit for someone with a singular, high-value objective. If you have received a firm quote for a roof replacement or want to consolidate $30,000 of high-interest debt into a more manageable structure, the fixed nature of this loan is ideal. It suits the “set it and forget it” personality—someone who wants a clear repayment schedule and no surprises.

A HELOC is often better suited for the strategic borrower. This might be a parent who needs to pay college tuition installments over several years or a homeowner who does a lot of their own repair work and needs to buy materials sporadically. Many regional institutions, offer these types of flexible credit lines to local homeowners looking for project-based funding.

Who Should Be Cautious or Avoid It

If you are already struggling to balance your monthly budget, adding a second lien to your home is rarely the solution. Borrowers should avoid these products if they intend to use the money for “wants” rather than “needs.” Financing a vacation, a luxury car, or a wedding with home equity means you will be paying for those temporary experiences for the next 10 or 15 years—long after the event has passed.

Additionally, if you plan to sell your home in the near future, you should be wary. The costs of setting up the loan might not be recouped in such a short window. There is also the risk that if the market dips, the combined total of your mortgage and your equity loan could exceed the sale price of the home, leaving you in a position where you owe money to the bank just to move out.

Alternatives to Consider

Before committing your home as collateral, it is worth exploring other avenues:

- Cash-Out Refinance: If interest rates have dropped since you got your original mortgage, you might replace your entire mortgage with a new one for a higher amount, pocketing the difference.

- Personal Loans: These are “unsecured,” meaning they aren’t tied to your home. While the interest rates are higher, the application process is faster and your house isn’t at risk if you default.

- 401(k) Loans: Some retirement plans allow you to borrow against your own savings. You pay the interest back to yourself, though there are strict rules regarding repayment if you leave your job.

- Consolidation Programs: For specific types of debt, you may find targeted solutions which may offer an alternative to using home equity. Some modern platforms like What Is TraceLoans.com? Debt Consolidation Review also explore digital debt restructuring solutions that may reduce the need to borrow against home equity.

Frequently Asked Questions

1. Can I get a home equity product if I have a low credit score?

While some specialized lenders work with lower scores, most traditional banks require a score of 680 or higher for competitive rates. A lower score usually results in a significantly higher interest rate or a lower borrowing limit.

2. How long does the approval process take?

Because these products require a home appraisal and a thorough title search, the process is much slower than a credit card application. It typically takes between two and six weeks from application to funding.

3. What happens if I sell my home before the loan is paid off?

When you sell your house you have to repay your Home Equity Loan or HELO. The balance is normally deducted by the closing agent with the sales proceeds.

4. Are there any restrictions on how I use the money?

Generally, no. Once the funds are in your hands, you can use them for anything from medical bills to home repairs. However, as mentioned earlier, the tax deductibility of the interest is strictly limited to home improvement projects.

Conclusion

Choosing between a Home Equity Loan and a HELOC is a matter of matching the financial tool to the specific task at hand. The Home Equity Loan offers the safety of a fixed path, while the HELOC provides the flexibility of a safety net. Both, however, represent a serious commitment of your home’s value. By understanding the structural differences and being honest about your own spending and repayment habits, you can utilize your home equity to strengthen your financial position rather than jeopardize it.