Velocity banking has emerged as a provocative strategy for homeowners and debt-conscious individuals looking to bypass the traditional thirty-year grind of a mortgage. Rather than simply sending a check to a lender every month and hoping for the best, this method reimagines how cash moves through a household. At its foundation, velocity banking involves using a revolving line of credit—most often a Home Equity Line of Credit (HELOC)—as a central financial hub to cancel out interest on amortized loans.

The strategy is less about “finding” new money and more about changing the “velocity” or movement of existing income. By treating a credit line like a checking account, proponents argue that they can lower the average daily balance of their debts, thereby reducing interest charges and accelerating the path to full ownership. However, beneath the surface of this mathematical approach lies a complex set of risks. This article provides an objective, deep-dive into the mechanics, potential rewards, and significant dangers of the velocity banking model.

What Is Velocity Banking?

At its simplest level, velocity banking is a debt-reduction technique where a borrower uses a revolving credit tool to pay down a non-revolving, amortized loan. While most people use a standard checking account to pay their bills, velocity banking practitioners substitute that account with a HELOC or a substantial personal line of credit (PLOC).

The term “velocity” describes the speed and frequency with which money enters and exits the credit line. Instead of letting cash sit in a traditional savings account earning negligible interest, that money is immediately applied to a debt balance. This reduces the principal faster than a standard payment schedule would allow. It is a shift in mindset: moving from a “static” banking model where money sits still, to a “dynamic” model where every dollar is put to work against interest-bearing debt the moment it is earned.

How the Strategy Works

The execution of this strategy is cyclical and relies on the specific way interest is calculated on different types of debt. While mortgages use monthly amortization, revolving lines of credit typically calculate interest based on an average daily balance.

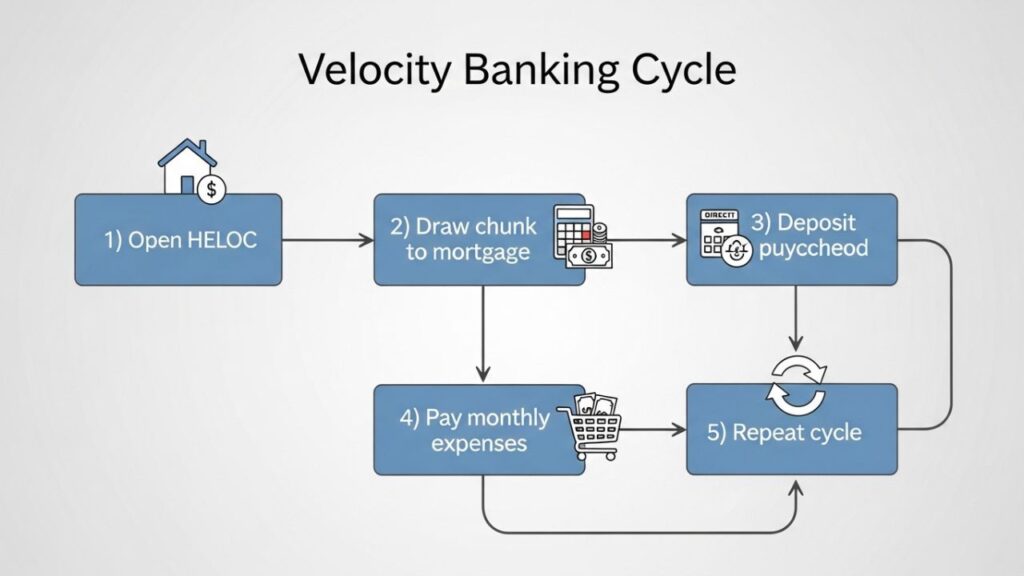

- Securing the Instrument: The first step is obtaining a revolving line of credit. A HELOC is preferred because it usually offers lower interest rates. If you’re unsure how a HELOC compares to other borrowing options, read Home Equity Loan vs HELOC: What’s the Difference? to understand the key differences and choose the right structure.

- The Principal “Chunk”: Once the credit line is open, the borrower makes a “chunk” payment toward their mortgage. For instance, if someone has a $200,000 mortgage, they might draw $10,000 from their HELOC to pay down the mortgage principal. This immediately lowers the amount of interest the mortgage company can charge.

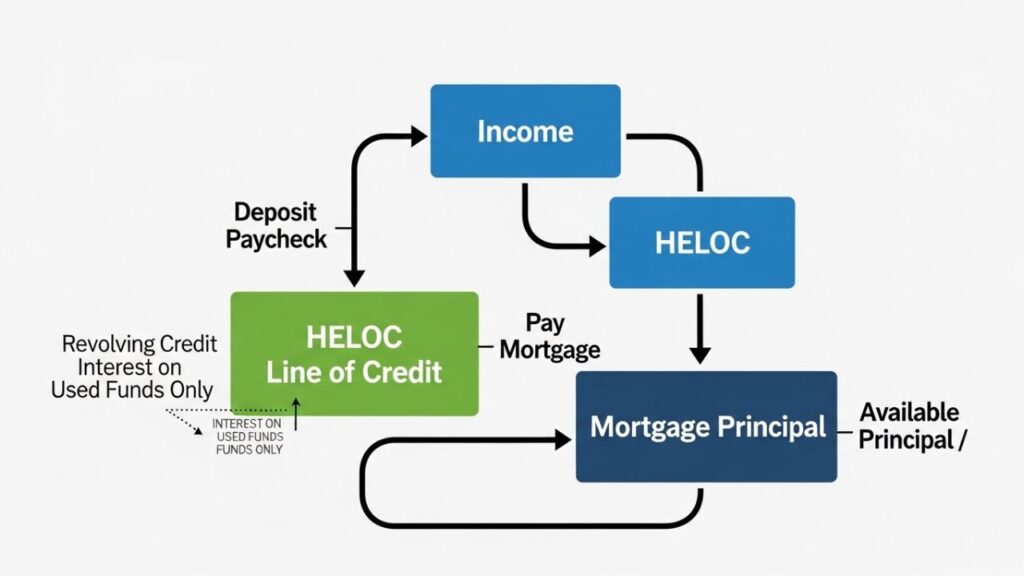

- Direct Deposit (Paycheck Parking): This is where the daily management begins. The borrower directs their entire monthly income—salary, bonuses, and side-hustle earnings—straight into the HELOC. Some people utilize a Salary Saving Scheme to manage their funds, but in velocity banking, the focus is on the credit line balance.

- Managing Monthly Outflow: Throughout the month, the borrower uses the HELOC to pay for all necessities.

- Capturing the Spread: This “positive cash flow” slowly whittles down the $10,000 chunk. Once that balance is gone, the borrower takes another $10,000 chunk from the HELOC and applies it to the mortgage, repeating the cycle.

Key Features and Core Components

To understand why this strategy attracts so much attention, one must look at the technical components that make the math function.

- Average Daily Balance: This is the primary driver of velocity banking. By parking a full paycheck in the HELOC at the start of the month, the average balance over thirty days is lower than if the money were deposited incrementally.

- Front-End Interest Mitigation: Traditional mortgages are designed so that the majority of early payments go toward interest rather than principal. By making large principal “chunks” early on, you effectively “skip” months of interest-heavy payments.

- Digital Integration: Successfully managing this strategy often requires high-tech banking interfaces. Understanding secure online systems is essential for protecting your digital assets while moving money frequently between accounts—What Is WebWise Banking? Features & Online Security Guide explains how to safely manage these transactions.

Potential Benefits and Advantages

When executed with precision, velocity banking offers a few distinct advantages over standard debt-repayment plans.

Significant Time Savings

By aggressively attacking the principal balance, homeowners can potentially cut a thirty-year mortgage down to ten or fifteen years. This acceleration is achieved without necessarily increasing the household budget, but rather by optimizing how the current budget is routed through different accounts.

Reduction in Total Interest Volume

The total “volume” of interest refers to the actual dollar amount paid over the life of a loan. By lowering the principal balance early, the borrower ensures that every subsequent monthly mortgage payment has a larger impact on the principal, creating a compounding effect of savings.

Flexibility and Emergency Access

One of the main deterrents to paying off a mortgage early is the fear of becoming “house rich and cash poor.” With velocity banking, funds remain accessible. This flexibility can be useful when managing other obligations, such as student debt; for those reviewing their existing debt terms, looking into TraceLoans.com Student Loans can help determine which debts should be prioritized.

Risks, Drawbacks, and Limitations

Despite the mathematical allure, velocity banking is fraught with variables that can turn a “wealth-building” strategy into a financial burden.

The Volatility of Variable Rates

Almost all HELOCs come with variable interest rates. If the economic climate changes and interest rates climb, the cost of carrying the balance on your HELOC could skyrocket. Borrowers unfamiliar with how revolving home-equity credit works can review the Investopedia HELOC Guide to better understand how HELOC interest structures, repayment periods, and variable-rate risks function before attempting a velocity banking strategy.

The Threat of “Line Freezes”

A revolving line of credit is a product controlled by a bank. In a recession, banks often freeze HELOCs to mitigate their own risk. If you have been parking your income in your HELOC and the bank suddenly freezes your ability to withdraw funds, you could find yourself unable to pay for basic necessities like utility bills.

Behavioral Risks and Discipline

The biggest point of failure in velocity banking isn’t the math—it’s the human element. This strategy requires the borrower to treat a credit line with extreme care. If the sight of a large available credit limit leads to impulsive purchases on sites, the borrower will quickly find themselves underwater.

Who It May Be Suitable For

Velocity banking is not a universal solution; it is a specialized tool for a very specific type of consumer. It is generally most effective for:

- High-Income Earners with Low Expenses: The strategy lives and dies by “cash flow.” If you have a $2,000 monthly surplus, the HELOC balance will drop quickly.

- The Financially Meticulous: This is for the person who keeps a detailed spreadsheet. Precision is mandatory to ensure that the “chunks” being taken out are sustainable.

- Stable Earners: For those with consistent income, local institutions often provide the stability and personal service needed to manage these frequent transfers.

Who Should Be Cautious or Avoid It

- People with Debt-to-Income Issues: If you are already struggling to make ends meet, adding a revolving credit line into the mix is dangerous.

- Those Impacted by Legal Issues: If your credit score has been damaged by events like a Credit One Bank Settlement, you may not qualify for the low-interest revolving lines required for this strategy.

- Inconsistent Earners: If your income fluctuates, you may find yourself in a month where you cannot “fill” the HELOC back up, causing interest to compound against you.

Alternatives and Related Options

If the risks of velocity banking seem too high, there are simpler ways to achieve similar results.

Automated Extra Principal Payments

Most mortgage servicers allow you to set up a recurring “principal-only” payment. Even adding a small amount each month to your principal can shave years off a mortgage without the risk of a “line freeze.”

Debt Consolidation

For those with multiple high-interest debts, using TraceLoans Debt Consolidation may be a more straightforward way to lower interest rates and simplify payments than implementing a complex velocity banking system.

Frequently Asked Questions

1. Is velocity banking a scam?

No, it is a legitimate financial strategy based on the math of interest calculation. However, the risks are often downplayed by those selling coaching programs.

2. Can I do this with a credit card instead of a HELOC?

While some attempt a version of this using credit cards, it is much riskier. Credit cards typically have much higher interest rates that usually make this strategy impossible to execute profitably.

3. Does velocity banking hurt my credit score?

It can. Using a large portion of your available credit line increases your “credit utilization ratio,” which may temporarily lower your score.

4. Can I use this for religious or alternative loan structures?

Yes, some individuals apply these principles to specific products like a Heter Iska Loan, which manages interest and profit-sharing differently than standard amortized mortgages.

Conclusion

Velocity banking offers a unique perspective on debt management, emphasizing the use of revolving credit to gain a mathematical edge over traditional amortization. By focusing on the average daily balance and the aggressive reduction of principal, it provides a structured path to early homeownership. However, the strategy is inherently tied to the stability of the housing market and interest rates. For the disciplined homeowner with substantial cash flow, it can be a powerful tool; for the average consumer, traditional methods remain a safer and more predictable alternative.