For decades, the Automated Teller Machine (ATM) has served as a cornerstone of modern banking, offering a bridge between physical branch locations and the digital management of personal finances. What began as a simple mechanism for dispensing cash has transformed into a sophisticated network of terminals capable of handling complex financial tasks. As consumer demand for convenience grows, these networks have evolved to include Interactive Teller Machines (ITMs), which provide a more personalized touch to the automated experience. By examining the infrastructure of a regional provider like trustmark atm, we can better understand how these systems maintain liquidity and security for the average account holder. Choosing the right financial setup also plays a key role in how effectively users interact with these systems. Learn more in How to Choose the Right Bank Account for Your Needs.

What Is the ITM Network?

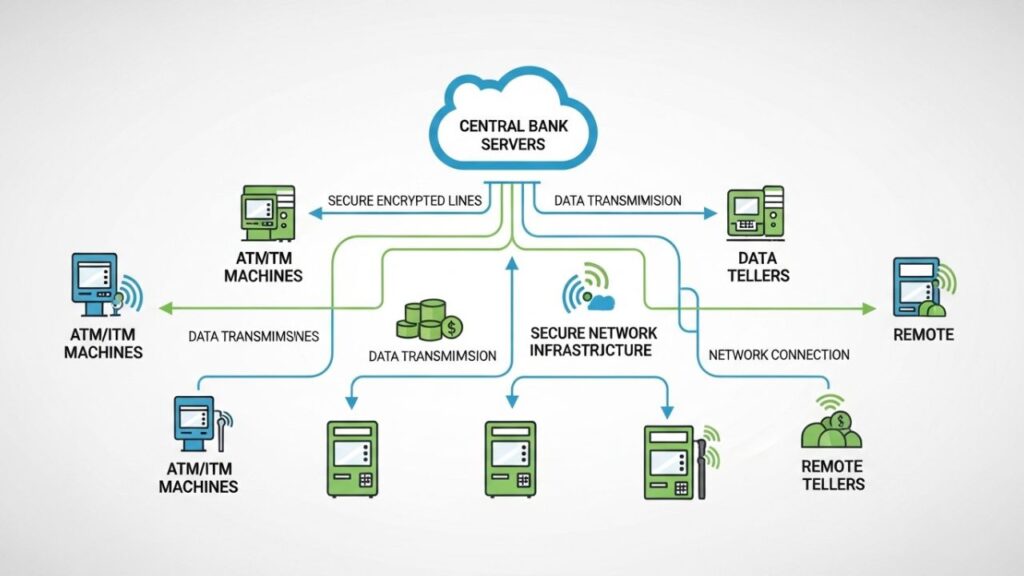

In technical terms, an ATM network is a secure telecommunications system that links individual terminals to a financial institution’s central data processor. This connection allows for real-time updates to account balances and the immediate distribution of funds. Trustmark manages a multi-tiered network that includes both traditional ATMs and “MyTeller” Interactive Teller Machines.

A normal ATM follows a pre-programmed software to handle transactions such as checking balance or withdrawing money, whereas an ITM has live video conferencing. This option enables customers to be able to talk to a remote teller live. Banks install these machines in drive-through lanes and kiosks so customers can access their savings or checking accounts 24 hours a day using a debit card or ATM card.

How ATM Networks Work: Behind the Screen

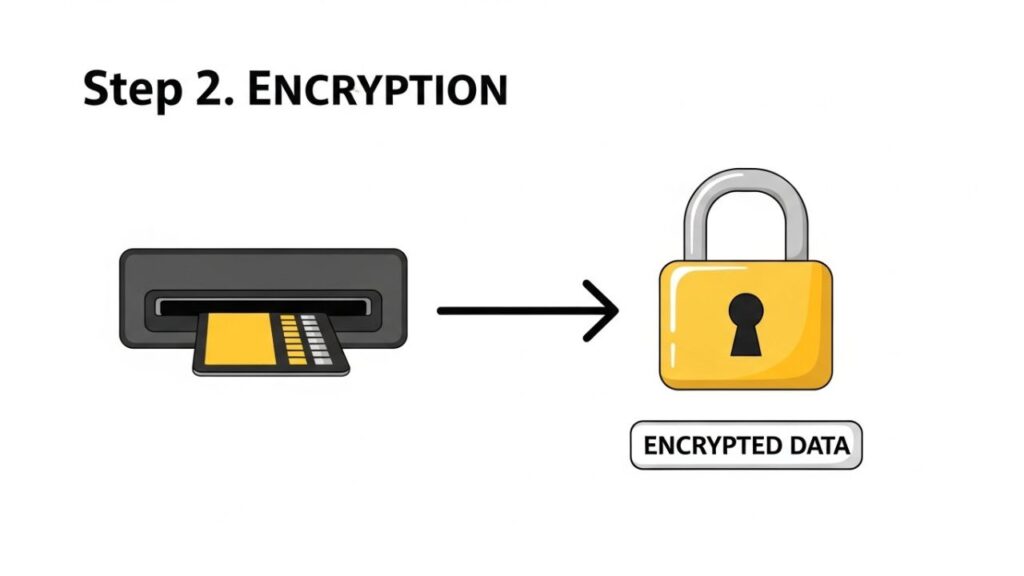

When you insert a card into a machine, a high-speed, encrypted dialogue begins between the terminal and the bank’s internal servers.

- Identity Verification: The process starts when the machine’s reader scans the EMV chip or magnetic stripe on your card. This identifies your specific bank and the encrypted data associated with your identity.

- Secure Routing: After you enter your Personal Identification Number (PIN), the terminal encrypts this sensitive information. This level of protection is part of a broader shift toward secure digital banking practices that protect users across all platforms. Read more in What Is WebWise Banking? Features & Online Security Guide It then sends a request through a “switch,” which acts as a digital traffic controller, routing the data to the correct financial institution.

- Real-Time Authorization: The bank’s processor receives the request and immediately checks two things: that the PIN is correct and that the account holds enough money to cover the request. It also runs a quick check against known fraud patterns to ensure the card hasn’t been stolen.

- Confirmation of Funds: Once the bank approves the transaction, it sends an authorization code back to the terminal. This message provides the “green light” for the hardware to proceed with the specific request, whether that is dispensing cash or accepting a check.

- Mechanical Execution: Inside the machine, a high-precision counting mechanism pulls the exact number of bills from a secure vault and delivers them to the dispenser. A digital record of the event is finalized, and the terminal generates a receipt to document the transaction for your records.

Key Features and Core Components

Modern banking terminals are far more than just “boxes of cash.” They are built with specialized hardware designed to withstand heavy use and prevent unauthorized access to data.

- Advanced Chip Readers: Most modern terminals prioritize EMV chip technology over the older magnetic stripe method. This shift is a direct response to “skimming” risks, as chips are much harder for criminals to duplicate.

- Smart Deposit Scanners: Modern units often utilize “envelope-free” technology. These machines use sophisticated optical character recognition (OCR) to read the numerical values on checks and high-speed sensors to verify the authenticity of cash deposits.

- Proximity Sensors and Contactless Tech: Some ITMs are now equipped with Near Field Communication (NFC) pads. This allows a user to simply tap their phone or a contactless card to begin a session, reducing wear and tear on the machine and speeding up the process.

- Interactive Video Hubs: Unique to the My Teller system is a high-definition video interface. This component includes a camera, microphone, and private handset, allowing users to handle tasks that a standard ATM cannot, such as cashing a check down to the exact penny or discussing a complex transfer with a live person.

Benefits and Advantages of Modern Networks

The most significant benefit of an expansive ATM and ITM network is the liberation of banking from the traditional “banker’s hours.” Historically, if you needed to deposit a check or withdraw cash after 5:00 PM, you had to wait until the following morning. Today, drive-through ATMs provide 24/7 liquidity, allowing users to manage their money on their own schedule.

The introduction of ITMs adds more flexibility to banking services. Tellers operate these machines from a central hub, so they can offer service hours beyond normal branch closing times. Customers get human assistance while still enjoying the speed of a self-service kiosk. Automated counting technology also reduces errors during deposits.

Risks, Drawbacks, and Limitations

Despite the high level of convenience, using an ATM or ITM involves certain trade-offs and risks that require a cautious approach.

- Security Vulnerabilities: Criminals sometimes install “skimmers” or hidden cameras on the exterior of a machine to capture card data and PINs. It is vital for users to visually inspect the card slot and keypad for any loose or unusual attachments before beginning a transaction. The Federal Deposit Insurance Corporation provides detailed guidance on ATM and debit card skimming schemes and how consumers can protect themselves from these types of fraud.

- Strict Withdrawal Caps: The majority of financial institutions impose a maximum ATM cash draw upon daily basis. The limit will safeguard the customers in case a card gets lost, but it can cause issues when one requires thousands of dollars to make an emergency purchase.

- Operational Failures: Like any piece of complex machinery, an ATM can break down. Mechanical jams, software updates, or power outages can render a machine useless, potentially leaving a user without access to cash when they need it most.

- Availability of Funds: While cash deposits are often credited to an account immediately, check deposits are a different story. Banks may place a “hold” on a check for several business days to ensure it clears from the issuing bank. Users should never assume that a deposited check will be available for immediate withdrawal.

Who It May Be Suitable For

ATM and ITM services are designed for the majority of personal banking customers who value efficiency. They are particularly well-suited for:

- Professionals who work irregular hours and cannot visit a bank during the day.

- Individuals who prefer the privacy of a self-service terminal over standing in a lobby line.

- People who frequently use cash for small purchases and need a reliable way to get money without incurring “out-of-network” surcharges.

Who Should Be Cautious or Avoid It

There are certain scenarios where a physical machine is not the best tool for the job.

- Commercial and Small Business Owners: If you have a large volume of cash from a day’s sales, the deposit limits of an ATM may be too low. In these cases, using a commercial night-drop box or visiting a teller in person is more appropriate.

- Privacy-Conscious Individuals in High-Traffic Areas: If an ATM is located in a poorly lit or overly crowded area, it may be safer to skip it. People who are concerned about “shoulder surfing”—where someone watches you enter your PIN—should stick to indoor machines.

- Complex Account Issues: If you need to dispute a transaction, open a new account, or apply for a loan, an ATM cannot provide the level of depth required. These situations necessitate a sit-down meeting with a bank officer.

Frequently Asked Questions

1. Can an ITM do everything a regular teller can do?

While ITMs are very capable, they cannot perform every task. They are excellent for deposits, withdrawals, and transfers, but they cannot issue new debit cards or handle complex loan applications.

2. How do I know if a machine is a Trustmark ATM or part of a different network?

Look for the official logo on the machine’s exterior and on the digital screen. Using a machine that does not match your bank’s logo may result in fees from both the machine owner and your own bank.

3. What happens if an ATM “eats” my card?

If a machine malfunctions and fails to return your card, do not leave the machine. Immediately call the customer service number listed on the terminal or use the bank’s mobile app to “freeze” your card so no one else can use it.

4. Is there a fee to talk to a teller through an ITM?

Usually, account holders do not pay an extra fee to speak with a teller through a MyTeller ITM, but they should still check their account’s fee schedule to confirm.

Conclusion

The modern ATM and ITM network is a testament to how technology can make daily life more manageable. By providing a secure, 24/7 gateway to financial accounts, these systems allow for a level of flexibility that was once unthinkable. However, the convenience of these machines comes with the responsibility of staying informed about security risks and understanding the physical limits of the hardware. Whether you are using a standard ATM for a quick withdrawal or engaging with an ITM for a more detailed transaction, these tools remain an essential part of a healthy and modern financial life.