The modern banking landscape relies heavily on alphanumeric codes and abbreviations to categorize transactions, manage automated payments, and maintain security protocols. For many account holders, these strings of characters appear on monthly statements without immediate explanation, often sparking confusion or concern regarding the safety of their funds. One such abbreviation that frequently appears in digital ledgers is ADTQ.

If you’re unfamiliar with how transaction codes appear on your statement, it’s helpful to first understand the basics by reading How to Read a Bank Statement (Beginner Guide). When a code like what is adtq in my bank account surfaces, it serves as a vital indicator of either a recurring service payment or a bank-initiated security prompt. By decoding these labels, consumers can distinguish between legitimate automated deductions and potential unauthorized activity. This guide provides an in-depth look at what ADTQ represents, how it functions within various banking systems, and the practical steps a consumer should take when they encounter it.

What Is ADTQ?

In the professional world of retail and commercial banking, ADTQ is a transaction descriptor or notification code. It is primarily utilized to identify specific types of electronic fund transfers or to flag a transaction that requires customer review. Because banking software architecture varies significantly by region and institution, the exact meaning of this string can shift slightly depending on where you hold your account.

Most commonly, ADTQ is associated with ADT Security Services. When a customer enrolls in an automated payment plan, such as the “ADT EasyPay” system, the banking software often truncates the merchant name to fit a standardized character limit. Additionally, certain international institutions, such as the National Australia Bank (NAB), utilize ADTQ as a shorthand notification. In this context, it acts as a digital nudge, alerting users to check their transaction history for recent online activity or unexpected deductions that may require manual authorization.

How It Works

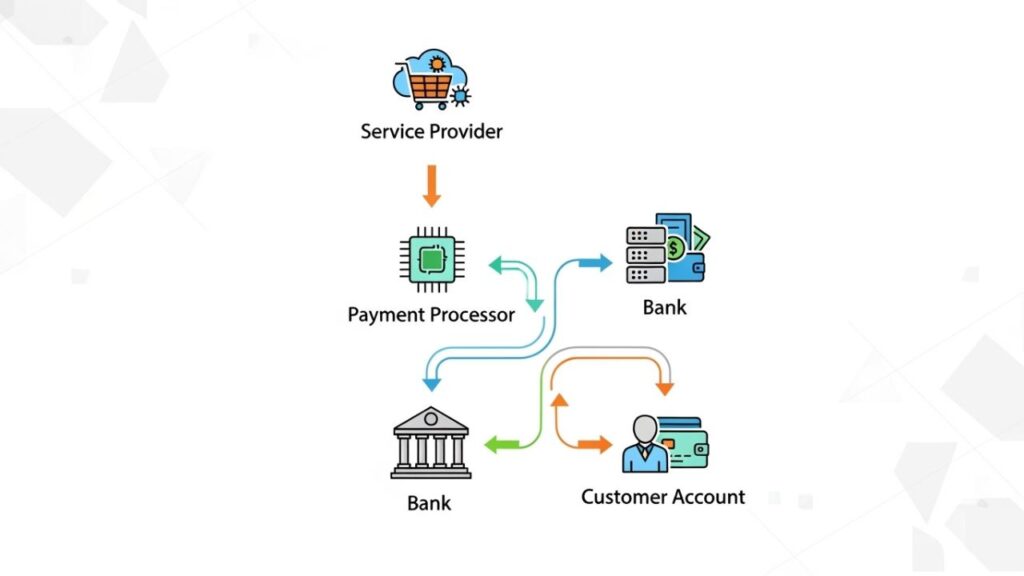

The appearance of ADTQ on a bank statement is rarely an isolated event; rather, it is the final step in a coordinated process involving a service provider, a payment processor, and your financial institution. Understanding the lifecycle of this code can help demystify its presence on your ledger.

- The Authorization Phase: The process begins when an account holder grants a “continuous payment authority” or signs a direct debit mandate for a service provider, most often a home security firm.

- The Electronic Request: On a predetermined billing date, the service provider’s financial institution sends an electronic request for funds to the customer’s bank through a centralized clearinghouse.

- Data Compression and Truncation: Older banking systems often possess inflexible character limit which limits the length of a transaction description thus abbreviates the name of the merchant. As an illustration, they tend to abbreviate such titles as ADT Security Quarterly or ADT Quick-Pay down to four letters ADTQ.

- Security Algorithm Flagging: In a secondary scenario, if a bank’s internal monitoring system detects an unusual spending pattern, it may attach the ADTQ code to a pending transaction. This serves as a “status flag” for the customer to verify the legitimacy of the movement of funds.

- Statement Rendering: Once the bank finalizes and posts the transaction, it prints the code on the physical or digital statement as the main reference for that financial event. This is important if your account has insufficient funds when the automated request occurs.

Key Features and Core Components

To identify ADTQ correctly among a sea of other transaction data, it is helpful to recognize the specific components that usually accompany it.

- Merchant Metadata: While “ADTQ” is the primary identifier, it is almost always followed by a unique string of numbers. These digits typically represent a customer’s specific contract number or internal account ID with the service provider.

- Transaction and Posting Dates: A standard entry shows two dates. The transaction date shows when the payment started, while the posting date shows when the bank moved the money.

- Recurring Frequency Patterns: Security subscriptions tend to make use of this code hence the transactions are made at a regular period. When you encounter the same code on a 30 days, 90 days, or 365 days basis, then it would most likely be a valid subscription.

- Platform-Specific Display: The code is most prevalent in mobile banking apps and online portals. These digital interfaces prioritize brevity, making truncated codes like ADTQ more common than they might be on a full-page, traditional paper statement.

Benefits and Advantages

While banking codes can feel cryptic, the use of standardized descriptors like ADTQ offers several functional advantages for the modern consumer.

The seamless automation is one of the benefits. The ADTQ code is used by people to pay their monitoring bills on a regular basis. This assists in avoiding the default of payments and ensures that there are home or business security systems in operation.

Furthermore, these codes contribute to enhanced organized record-keeping. By using a specific, searchable string of text, the banking system simplifies the process of auditing one’s own finances. This level of clarity is similar to how a professional consultant en finances might organize a client’s ledger. If a user needs to determine their total annual expenditure on home safety, they can simply search their banking app for “ADTQ” to see a chronological list of all related costs.

Risks, Drawbacks, and Limitations

Despite the operational efficiency of automated coding, there are significant risks and honest limitations that every account holder should acknowledge.

In some cases, unclear or suspicious transaction codes can even trigger account restrictions or temporary holds, similar to situations explained in What Happens When a Bank Freezes Your Account? Because ADTQ is not a globally universal standard, its meaning can be misinterpreted. For instance, some users may confuse it with “ATF” (As Trustee For). While ADTQ usually signifies a payment for a service, ATF relates to the legal structure of a trust account.

Another concern is the lack of transparency for the layperson. A four-letter acronym provides almost no context regarding the nature of the charge. This lack of clarity can be exploited; if a fraudulent entity uses a similar-looking descriptor, a busy account holder might gloss over the entry. This “hidden in plain sight” strategy allows unauthorized small-dollar deductions to persist for months. It is always wise to verify if a site or service is legitimate, before sharing financial details.

Who It May Be Suitable For

The ADTQ transaction framework is primarily designed for those who value efficiency and consistency in their financial lives. It is most suitable for:

- Subscribers to Professional Services: Homeowners with active monitoring contracts who prefer to avoid the hassle of manual monthly payments.

- Digital-First Bankers: Users who primarily manage their money through mobile apps and appreciate a clean, uncluttered interface.

- Structured Budgeters: Individuals who prefer “fixed” costs that occur on a predictable schedule, allowing them to forecast their monthly outflows with high precision.

Who Should Be Cautious

Certain individuals should exercise a higher level of scrutiny when they encounter ADTQ or similar abbreviations on their ledgers:

- Non-Contract Holders: If you do not currently have a service agreement with a security firm, the appearance of ADTQ is a significant red flag. This could indicate a clerical error or potential fraud.

- Trustees and Fiduciaries: People managing funds on behalf of others must be exceptionally careful. Confusing a service deduction with a legal designation could impact complex financial holdings, such as a term finance certificate.

- Low-Balance Account Holders: For those managing tight margins, automated deductions can be risky. If an ADTQ charge hits the account before a deposit arrives, it could trigger fees.

Alternatives and Related Options

If an account holder finds automated codes like ADTQ to be too opaque or risky, there are several alternative methods for managing these types of payments:

- Electronic Bill Pay (Push Payments): Rather than allowing a company to “pull” money from your account, you can use your bank’s bill-pay feature. This gives you total control over the timing.

- Credit Card Integration: Moving recurring subscriptions to a credit card provides an additional layer of consumer protection.

- Virtual Card Numbers: Some modern financial institutions allow the creation of unique virtual cards for specific vendors. You can label these cards yourself, so instead of seeing a vague code, you see a custom note like “Security System Payment.”

Frequently Asked Questions

1. Does the ADTQ code always indicate that money has been deducted?

In most cases, yes, it represents a completed or pending payment. However, in certain banking environments, it may appear as a “zero-dollar” entry. In these instances, the code is functioning as a notification or a reminder for the customer to review their transaction logs.

2. Why did ADTQ appear on my statement if I usually see the full name of the company?

Banking organizations normally refresh their internal software. In such updates, they can modify the way statements present data. They can therefore abbreviate a name of a merchant previously found on a record to a collection of letters such as ADTQ.

3. Is there any connection between ADTQ and investment products?

No. It is important to clarify that ADTQ is strictly a banking transaction or notification descriptor. It is not a ticker symbol for a stock, nor is it related to complex structures like an [suspicious link removed].

4. What is the fastest way to resolve an unrecognized ADTQ charge?

The most effective approach is to first verify your own records for any security-related subscriptions. If the charge remains unidentified, contact your bank’s fraud or customer service department immediately to investigate the origin of the transaction.

Conclusion

The ADTQ code is a common feature of the modern, automated banking experience. While its appearance may initially seem obscure, it generally serves as a shortened label for a recurring service payment or a protective notification designed to prompt a review of account activity.

Navigating these codes successfully requires a balance of trust in automated systems and a commitment to personal vigilance. By understanding the origins of such descriptors, account holders can ensure their financial records remain accurate. Proper monitoring of these codes is a simple but effective way to maintain the health of your other comprehensive income and overall financial standing.