A steady income can be put to test by having to manage a number of monthly due dates and high interest rates. Debt consolidation is a method of coming together various high interest debts into a structured loan. This is primarily aimed at reducing the complexity of payments and possibly reducing the total cost. Although the concept is very straightforward, a single bill rather than numerous, its success lies in interest rates, charges, and expenditure patterns. The merger does not eliminate debt consolidation loans, it transfers it to an account and on different conditions. When put into proper use, it can contribute to financial recovery. It might form an even greater burden without transforming the core habits.

What is Debt Consolidation?

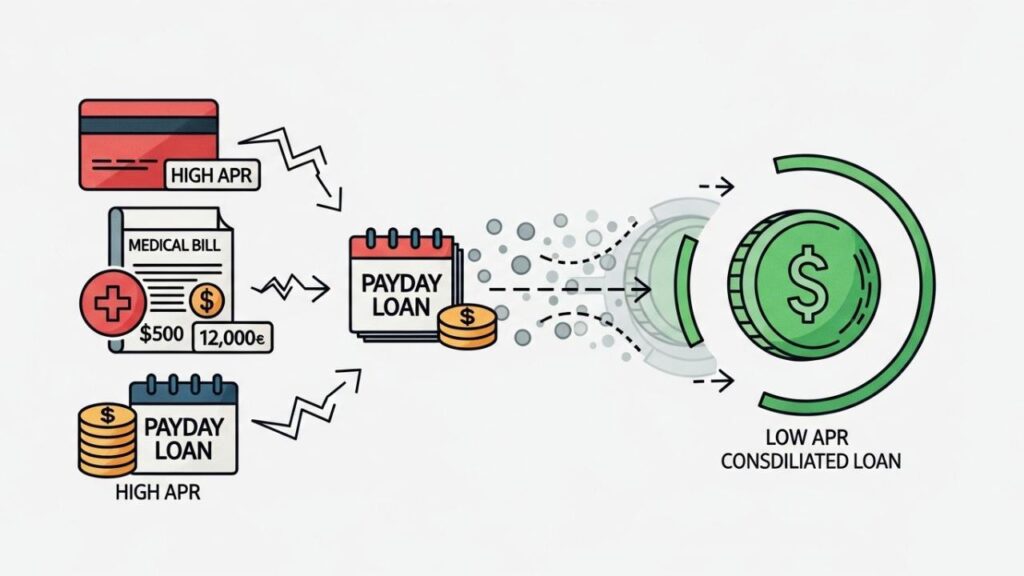

In plain terms, debt consolidation is the act of taking out a new loan to pay off several smaller, high-interest debts. Instead of managing a variety of payments for credit cards, medical bills, or payday loans, you deal with a single lender.

Ideally, this new loan carries a lower Annual Percentage Rate (APR) than the average of your previous debts. By securing a better rate, more of your monthly payment is applied to the principal balance rather than being lost to interest charges, allowing you to pay off the total amount more efficiently.

How Debt Consolidation Works

The journey from multiple bills to a single payment typically involves a logical, step-by-step progression:

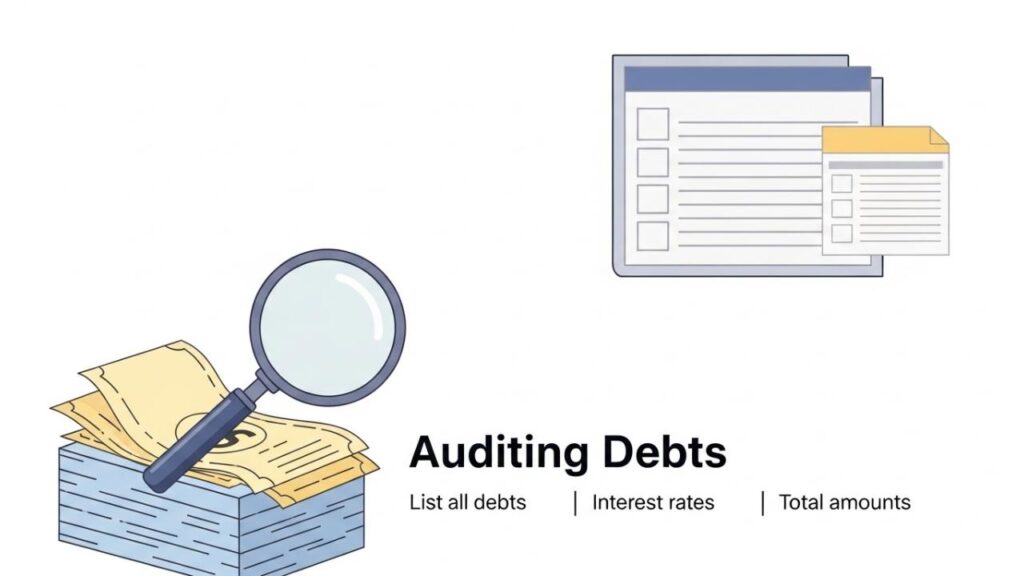

- The Audit: You begin by listing every outstanding debt, noting the total balance, the current interest rate, and the minimum monthly payment for each.

- The Comparison: You research lenders to see what interest rates you qualify for based on your current credit score and income.

- The Application: After identifying a lender with favorable terms, you apply for a loan equal to the sum of your existing debts.

- The Payout: If approved, the new lender may pay your creditors directly. Alternatively, they deposit the funds into your account for you to distribute to your various creditors yourself.

Key Features and Core Components

To evaluate whether a consolidation offer is truly beneficial, it helps to understand its fundamental mechanics:

- Fixed Interest Rates: Unlike credit cards, which often have variable rates that can climb unexpectedly, most consolidation loans offer a fixed APR for the life of the loan.

- Set Repayment Timeline: These loans usually come with a term of two to seven years, giving you a definitive “finish line” for your debt.

- Origination Fees: Many lenders charge a one-time processing fee (typically 1% to 12% of the loan amount). It is vital to factor this cost into your total savings calculation.

- Credit Utilization Shift: By moving “revolving” credit card debt into an “installment” loan, you can significantly lower your credit utilization ratio, which is often a catalyst for a higher credit score.

Benefits and Advantages

When executed under the right conditions, consolidation offers several clear advantages:

Streamlined Financial Life

Managing one due date is significantly easier than tracking five or six. This simplicity reduces the likelihood of human error, such as forgetting a payment or incurring late fees that further damage your credit.

Potential Interest Savings

The most compelling reason to consolidate is to lower your interest rate. If you can move debt from a 22% APR credit card to a 9% APR personal loan, you significantly reduce the “cost of borrowing,” keeping more money in your pocket over time.

A Clear Exit Strategy

Revolving debt can feel like a treadmill because there is no set end date. A consolidation loan provides a structured amortization schedule, ensuring that as long as you make the monthly payments, the debt will be gone by a specific date.

Risks, Drawbacks, and Limitations

It is a mistake to view consolidation as a “clean slate” without acknowledging the potential pitfalls.

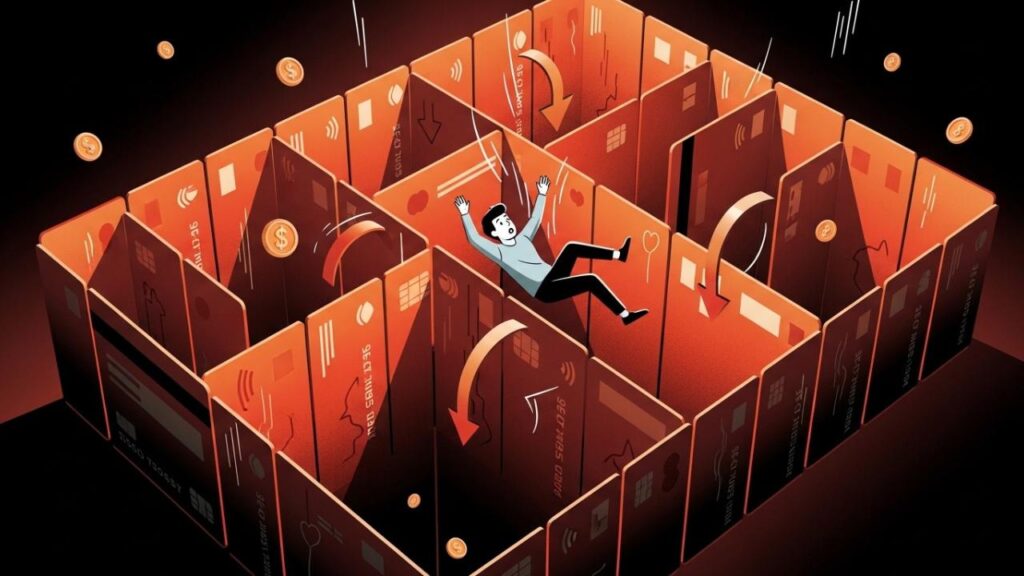

The Spending Trap

The most common failure in debt consolidation is behavioral. When credit card balances are zeroed out by a loan, those cards become available to use again. If a borrower continues to charge new purchases while paying off the consolidation loan, they may end up with twice as much debt as they started with.

Long-Term Interest Costs

A lower monthly payment is not always a win. If you extend your repayment period significantly—for example, moving a three-year debt into a seven-year loan—you might end up paying more in total interest over the life of the loan, even if the APR is lower.

Upfront Expenses

Between origination fees and potential “hard inquiries” on your credit report, the initial stages of consolidation have costs. You must ensure the long-term interest savings outweigh these immediate expenses.

Who It May Be Suitable For

This strategy is most effective for those who find themselves in a specific “financial sweet spot”:

- Individuals with Fair-to-Excellent Credit: The best rates are reserved for those with higher scores. If your credit has improved since you first took out your existing debts, you are a prime candidate for a better rate.

- Borrowers with a Consistent Income: Because consolidation loans require a fixed monthly payment, you need a reliable cash flow to ensure you don’t default.

- Those Ready for a Lifestyle Change: It is ideal for someone who has already identified why they went into debt and has implemented a budget to prevent it from happening again.

Who Should Be Cautious or Avoid It

In some cases, consolidation can actually hinder financial progress:

- Those with Deeply Damaged Credit: If your score is low, the interest rates offered by consolidation lenders might be just as high as your current credit cards, offering no real benefit.

- Small-Scale Debtors: If you can pay off your balances within a few months through aggressive budgeting, the fees and paperwork of a new loan are likely unnecessary.

- People Facing Insolvency: If your total debt is overwhelming and your income cannot cover a consolidation payment, you may need to explore debt relief programs or legal counsel regarding bankruptcy rather than taking on more credit.

Alternatives and Related Options

If a personal loan doesn’t seem right for your situation, consider these other paths:

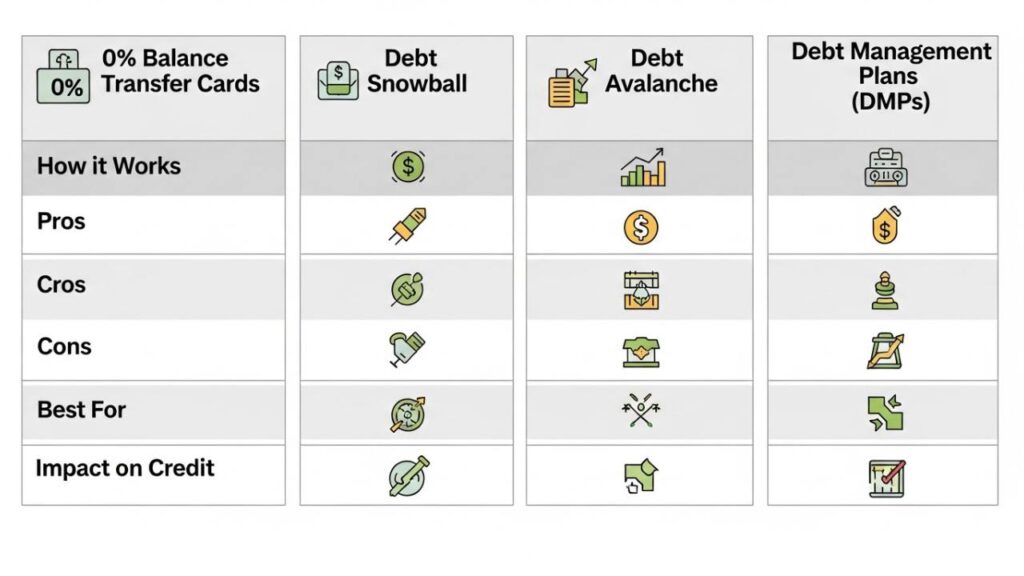

- 0% APR Balance Transfer Cards: These allow you to move debt to a new card with no interest for a promotional period. This is often the cheapest option if you can pay the balance before the promo expires.

- The Debt Snowball or Avalanche: These are “DIY” methods that involve prioritizing certain debts based on balance size or interest rate without opening new accounts.

- Non-Profit Credit Counseling: Agencies can set up Debt Management Plans (DMPs) that lower your interest rates through direct negotiation with creditors, often without requiring a new loan.

Strategic Considerations for Debt Management

- Institutional Accountability: Staying informed about legal developments, such as the OneMain Financial settlement, can provide context on consumer rights and how large lenders handle collections and compliance.

- Understanding Bank Fees: Before moving funds, verify the status of your accounts to avoid “hidden” costs. Knowing the implications of insufficient funds and how they trigger fees is vital for maintaining the liquidity needed for a new loan payment.

- Deciphering Statements: Many borrowers are confused by vague transaction codes during their financial audit. Identifying specific markers, such as ADTQ in a bank account, ensures you have a clear picture of where your money is going.

- Asset-Backed Debts: If your financial situation involves more than just consumer credit, such as inheriting a house with debt, consolidation becomes a more complex conversation involving equity and collateral.

- Verifying Platforms: For those considering digital tools to manage their transition, always verify the legitimacy of third-party portals, such as confirming if MyCardBenefits is a secure site for your specific credit card perks.

Frequently Asked Questions

1. Does debt consolidation close my old accounts?

The loan pays off the balance, but the accounts remain open unless you choose to close them. Keeping them open (but unused) is generally better for your credit score as it maintains your “age of credit.”

2. Can I consolidate all types of debt?

Most lenders allow you to consolidate unsecured debt like credit cards and medical bills. However, secured debts (like auto loans) or federal student loans are usually handled through different, specialized programs.

3. What happens if I miss a payment on a consolidation loan?

Because it is an installment loan, a single missed payment can significantly hurt your credit score and may trigger late fees. It is crucial to ensure the monthly payment fits comfortably within your budget.

4. Is a consolidation loan the same as debt settlement?

No. Consolidation is paying back 100% of what you owe under new terms. Settlement involves asking creditors to accept a partial payment, which can have a severe negative impact on your credit rating.

Conclusion

Debt consolidation is an organizational tool that can make the path to financial freedom much smoother. By trading high-interest, scattered payments for one predictable monthly installment, you gain both a lower cost of borrowing and a clear end date. However, the tool is only as effective as the person using it. For consolidation to work long-term, it must be paired with a commitment to living within a budget and a firm resolve to avoid accumulating new debt while the loan is being repaid.