In the sophisticated world of alternative investments, liquidity—the ease with which you can convert an asset into cash—is often the “hidden” variable that determines an investor’s experience. While most people are accustomed to the seamless, daily liquidity of the public stock market, private gating fund operate under a different set of architectural rules. One of the most significant, yet frequently misunderstood, mechanisms in these vehicles is the “gate.”

A gating fund is an investment vehicle—typically a hedge fund, private equity fund, or non-traded real estate investment trust (REIT)—that includes specific provisions allowing managers to temporarily restrict or halt investor withdrawals. These provisions act as a structural safety belt. By limiting the amount of capital exiting the fund during a specific window, managers aim to protect the fund’s overall stability and prevent a “run on the fund” during periods of heightened market volatility. Understanding how these gates function is a prerequisite for anyone considering semi-liquid or private market investments.

What Is a Gating Fund?

A gating fund uses a “redemption gate” to limit how much capital investors can withdraw at once. Unlike standard mutual funds with daily liquidity, these funds often hold illiquid assets—such as real estate or private loans—that are difficult to sell quickly.

The gate acts as a “speed bump” during market stress. If too many investors try to exit simultaneously, the manager can halt or restrict withdrawals to avoid a “fire sale” of assets at a discount. This mechanism protects the fund’s stability and ensures that remaining investors aren’t unfairly harmed by a sudden rush for the exits.

How It Works

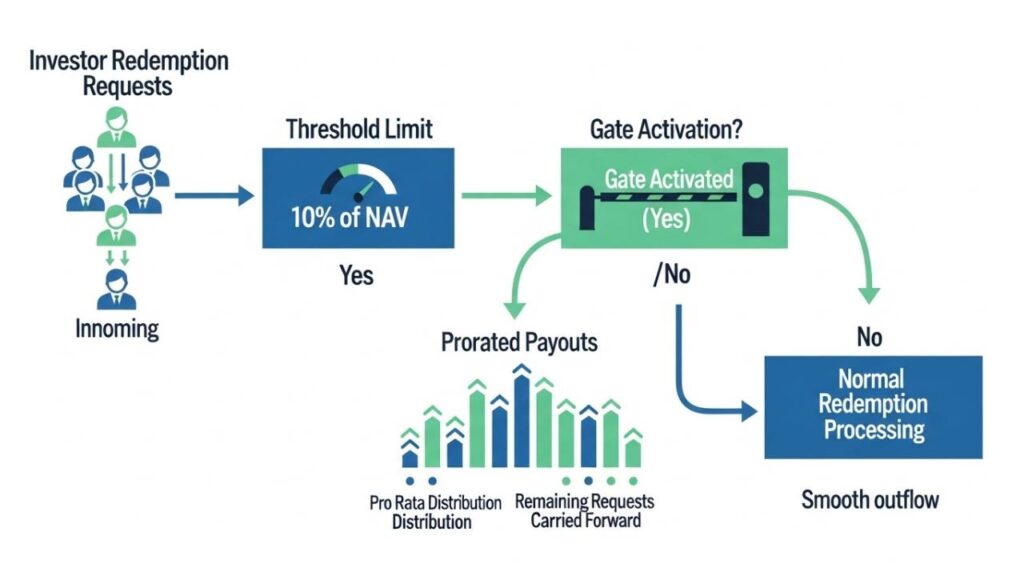

The manager triggers a gate following a specific sequence of events set in the fund’s legal offering documents. While every fund has its own nuances, the mechanism generally operates through the following steps:

- The Submission of Redemption Requests: Investors submit a formal notice during a specific window (usually quarterly or semi-annually) stating that they wish to withdraw a portion or all of their capital.

- The Threshold Assessment: The fund manager aggregates all these requests. Most funds have a pre-set limit, often around 5% of the fund’s total Net Asset Value (NAV) per quarter.

- The Activation Trigger: If the total volume of withdrawal requests exceeds the pre-set threshold (for example, if 10% of the fund’s investors want to leave but the limit is 5%), the manager officially “trips” the gate.

- The Proration of Capital: To maintain fairness, the manager distributes available cash proportionally. If the gate is 5% but requests reach 10%, the manager gives each investor only 50% of their requested cash.

- The Rollover Period: The manager rolls over any unfulfilled withdrawal to the next redemption period, subjecting it to the same liquidity checks and gate rules.

Key Features and Core Components

Gating mechanisms are rarely uniform. They are tailored to the specific type of assets the fund holds. These restrictions generally fall into two primary categories that dictate how an investor can access their money:

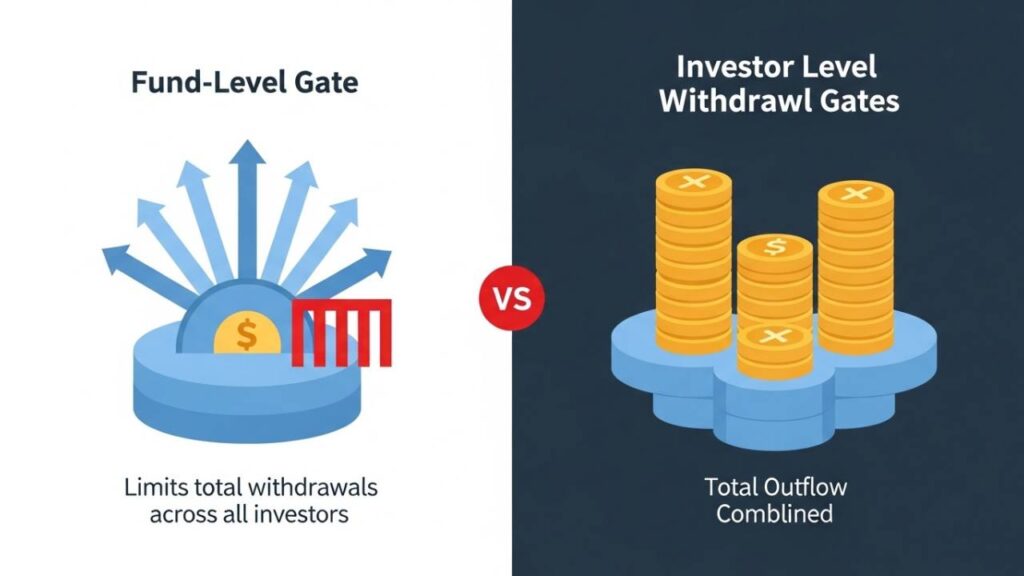

- Fund-Level Gates: These limits apply to the entire fund. If the manager sets a 2% quarterly gate, they allow only 2% of total assets to exit, no matter how many investors request withdrawals.

- Investor-Level Gates: These are more personalized. A fund might dictate that a single investor can only withdraw a specific percentage of their own holding (e.g., 25% per quarter). This prevents a single large institutional investor from draining the fund’s cash reserves and leaving smaller investors at a disadvantage.

- Hard Gates vs. Soft Gates: A “hard gate” is a strict, non-negotiable limit. A “soft gate” offers the manager more discretion. They might allow higher withdrawals, but they often charge a “redemption fee” to compensate the remaining shareholders for the extra liquidity cost.

Benefits and Advantages

While the idea of restricted access to one’s money may seem inherently negative, gating serves several vital functions that protect the long-term health of an investment:

- Prevention of “Fire Sales”: If a manager is forced to raise massive amounts of cash instantly, they must sell assets at whatever price they can get. These “fire sales” can destroy the value of the fund. Gates allow for an orderly disposal of assets at fair market prices.

- Maintenance of Strategy Integrity: Many complex investment strategies take years to succeed. If a fund liquidates positions during a temporary market panic, it undermines the strategy investors agreed to.

- Equity Among Shareholders: Without a gate, the first investors to “run” would get their cash at full value, leaving those who stayed behind to deal with the remaining, harder-to-sell assets. Gates ensure that the burden of liquidity is shared fairly across the entire investor base.

Risks, Drawbacks, and Limitations

The primary risk of a gating fund is liquidity risk, and it is a significant factor that investors must weigh against potential returns. When you enter a fund with a gate, you are essentially trading your flexibility for the potential of higher yields in private markets.

- Capital Lock-up: During a financial crisis, you might need your cash for personal or business emergencies. A gated fund traps capital, potentially for several quarters or even years.

- Opportunity Cost: A gated, underperforming fund traps your capital, preventing you from moving it into better investments or seizing new opportunities.

- Psychological Stress: Legal restrictions can bar you from exiting an investment while its value fluctuates, causing anxiety and a sense of powerlessness.

- Negative Market Signaling: Sometimes, the act of a fund “dropping the gate” can signal distress to the broader market. This can lead to a “death spiral” where the perception of trouble causes more investors to try to leave, keeping the gate closed even longer.

Who Should Be Cautious or Avoid It

Retail investors or those with limited savings should approach gating funds with extreme skepticism. You should likely avoid these structures if:

- You need “emergency fund” access: If the money you are investing represents a significant portion of your liquid net worth, the risk of a gate is mathematically too high to justify.

- You have a short time horizon: If you plan to buy a house, fund a wedding, or retire within the next three to five years, the potential for a multi-quarter lock-up is a deal-breaker.

- You prioritize daily control: If you prefer the ability to exit a position the moment a news headline breaks, the restrictions of a gate will be a source of constant frustration.

Alternatives or Related Options

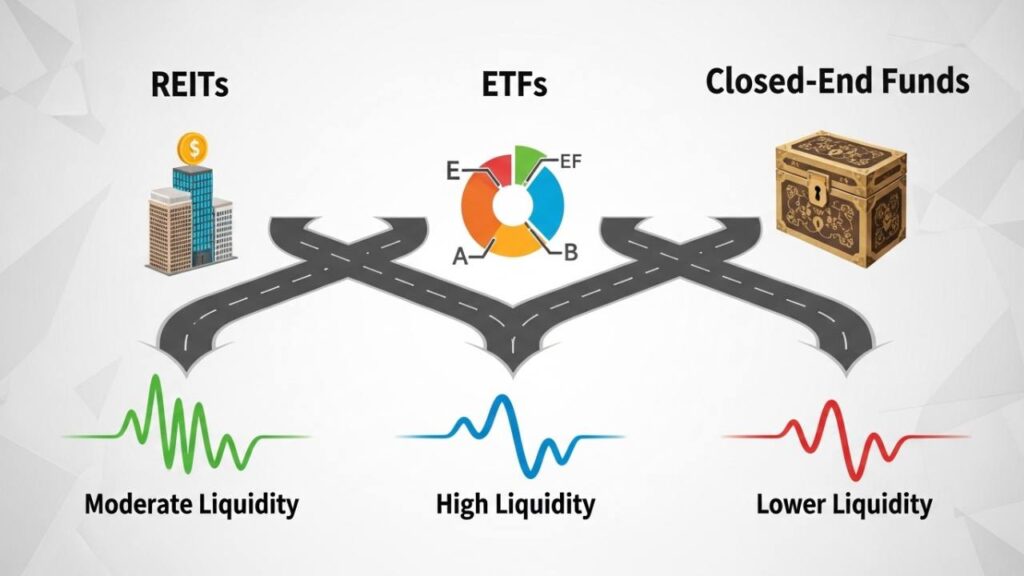

If you find the idea of a gate unappealing, several other structures offer different liquidity profiles for alternative assets:

- Publicly Traded REITs: These own real estate portfolios but trade on public exchanges like the New York Stock Exchange. They offer daily liquidity, though they tend to be more volatile.

- Exchange-Traded Funds (ETFs): Many modern ETFs track private equity or private credit themes while providing the ability to buy and sell shares every day the market is open.

- Closed-End Funds (CEFs): These funds have a fixed number of shares that trade on an exchange. While the underlying assets might be illiquid, you can sell your shares to another buyer on the open market, though often at a discount to the actual value of the assets.

Further Reading & Resources

To deepen your understanding of market liquidity and professional portfolio management, consider these essential concepts and tools:

- Market Analysis Tools: Explore how advanced trading platforms like Ape Pro help investors monitor real-time market settings and execute trades with precision.

- Asset Valuation: Learn the importance of an Asset by Asset review to determine the true underlying value of a fund’s holdings during redemption periods.

- Infrastructure & Growth: Discover how Fondion supports construction and project-based businesses that often require long-term, semi-liquid financing structures.

- Global Trading Standards: Stay informed on institutional initiatives like the Global Trader Programme to understand how international markets manage liquidity and cross-border capital flows.

Frequently Asked Questions

1. Does the activation of a gate mean the fund is going bankrupt?

Not necessarily. In fact, many of the world’s largest asset managers have used gates during periods of market stress. It is a tool designed to manage a mismatch between how fast investors want their money and how fast the assets can be sold. It is often a sign of prudent risk management rather than insolvency.

2. Can a manager keep a gate closed indefinitely?

No. The fund’s legal documents will outline the specific conditions and time limits for how a gate can be used. However, if the underlying market for the fund’s assets remains frozen for years, the gate can effectively remain in place for a long duration.

3. Will I still receive dividends or interest if a fund is gated?

In many cases, yes. While you may be unable to withdraw your “principal,” many funds continue to distribute the income generated by the underlying assets, such as rent from buildings or interest from loans.

4. How can I find out if my fund has a gate?

This information is located in the fund’s “Offering Memorandum” or “Prospectus” under sections typically labeled “Redemptions,” “Withdrawals,” or “Liquidity Provisions.”

Conclusion

A gating fund is a specialized investment structure designed to bridge the gap between long-term, illiquid assets and investor desire for capital. By slowing down the exit of capital during times of high volatility, these funds protect the collective interests of all shareholders and prevent the destructive “fire sale” of assets.

However, this protection comes at a price: the loss of immediate control over your capital. As with any investment, the key is transparency and alignment. Investors must ensure that the liquidity profile of the fund matches their personal financial needs and their ability to wait out market cycles. Understanding the “gate” before you enter the fund is the best way to ensure you aren’t surprised when you try to leave.