Gold has occupied a singular space in the global financial landscape for millennia. Unlike a paper currency, which derives its value from the stability and credit of a physical government, gold is a tangible asset with inherent properties that make it a perennial subject of interest for those looking to protect their capital. In the architecture of a modern investment portfolio, gold is rarely viewed as the primary engine for aggressive growth or wealth creation. Instead, it functions as a strategic tool for wealth preservation and a stabilizing force against systemic risk. As of March 2026, the Gold investment analysis market is navigating a particularly complex environment. While the long-term structural demand remains a focal point for institutional analysts, the asset has recently entered a period of notable price volatility.

Understanding the underlying mechanics, potential benefits, and inherent risks of gold is essential for any individual seeking to diversify their holdings. This article provides an objective, in-depth overview of how gold investment functions within a comprehensive, long-term financial strategy.

What Is Gold Investing?

At its most fundamental level, Gold investment analysis involves the acquisition of the precious metal in either its physical form or through sophisticated financial instruments that mirror its market value. Historically, gold served as the bedrock of global commerce under the “gold standard,” where currencies were directly convertible into a fixed amount of the metal. While modern fiat currencies are no longer backed by physical reserves in this manner, gold remains a “tier-one” reserve asset held by central banks across the globe.

In finance, investors classify gold as a non-yielding asset, meaning it does not produce dividends, interest, or rental income. Instead, its value comes from its limited supply, its use in industry and jewelry, and its strong reputation as a safe haven during economic or political uncertainty. For long-term investors, gold acts as financial insurance, helping protect wealth when other assets lose value.

How Gold Investment Works

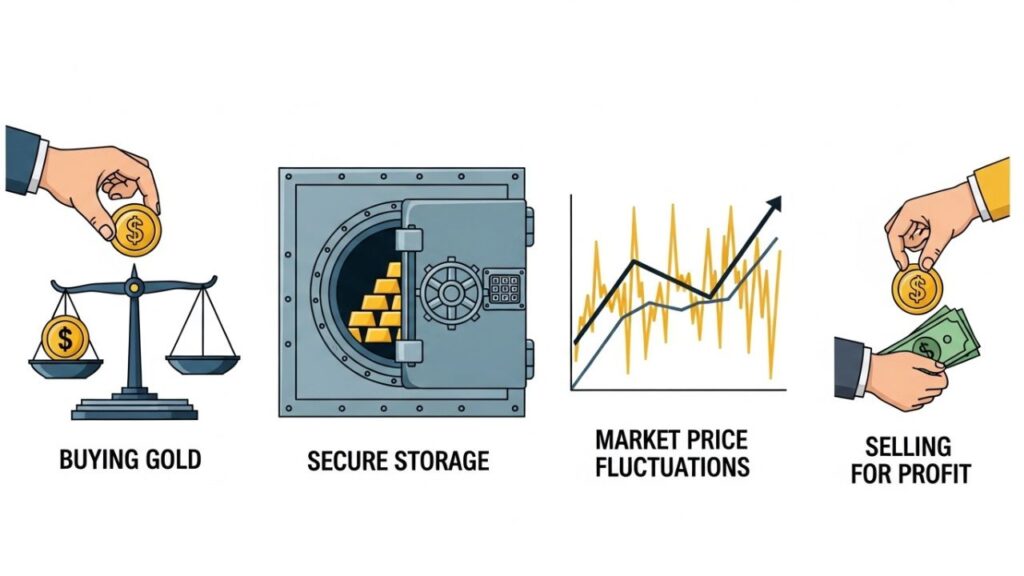

Entering the gold market can be approached through several distinct avenues, ranging from direct physical ownership to indirect market exposure through brokerage accounts.

- Selection of the Investment Vehicle: An investor must first determine the most appropriate method for their needs. This could involve purchasing physical bullion, investing in Gold Exchange-Traded Funds (ETFs), or buying shares in gold mining companies.

- Acquisition and Premium Pricing: Gold is traded continuously on global exchanges. The “spot price” represents the current market rate for one troy ounce. However, buyers of physical metal usually pay a “premium” over this spot price to cover the minting, refining, distribution, and dealer margins.

- Storage and Security Logistics: For those choosing physical gold, arrangements must be made for high-security storage. This might involve a home safe or a third-party professional depository. Digital platforms like WebWise Banking have made managing traditional financial accounts easier, but physical gold requires a more manual approach to security.

- Market Valuation Drivers: Once acquired, the value of the holding fluctuates based on global supply and demand. Key influences include the purchasing patterns of emerging market central banks and the relative strength of the U.S. Dollar.

- Liquidation and Exit: When an investor decides to rebalance their portfolio, the gold is sold back to a dealer. The final return is the difference between the purchase and sale price, after deducting all transaction and insurance expenses.

Key Features of Gold

Gold possesses several unique characteristics that distinguish it from traditional financial assets like stocks, bonds, or real estate.

- Finite Scarcity: Gold cannot be printed or manufactured at will. New supply from mining operations typically increases the global stock by only a tiny percentage each year.

- High Liquidity: Despite being a physical commodity, gold is among the most liquid assets globally. It can be converted into cash in almost any country at a price tethered to the global spot rate.

- Physical Durability: Gold is virtually indestructible. It does not rust or decay over time. This physical permanence is a major reason why societies have trusted it as a store of value for thousands of years.

- Low to Negative Correlation: Gold frequently moves independently of paper assets. When the equity markets face extreme downward pressure, gold frequently maintains its value or even appreciates.

Benefits of Investing in Gold

The primary motivation for incorporating gold into a wealth management strategy is diversification. Because gold often reacts differently to economic catalysts than stocks or corporate bonds, it can act as a “buffer,” smoothing out the overall volatility of a diversified portfolio during turbulent market cycles.

Another significant advantage is gold’s historical role as a hedge against currency devaluation. When a currency loses its purchasing power due to high inflation, the price of gold often rises in that currency’s terms. Furthermore, physical gold carries no “counterparty risk.” Unlike a bond, which relies on an issuer’s ability to pay, a gold bar’s value is not contingent on anyone else’s promise to perform. Some investors utilize a salary saving scheme to build up capital for such tangible assets over time.

Risks, Drawbacks, and Limitations

Anyone considering an allocation should be fully aware of the following challenges:

Significant Price Volatility

As demonstrated in the early months of 2026, the price of gold can be subject to sharp and sudden corrections. Factors such as a “hawkish” shift in Federal Reserve policy can trigger a mass sell-off. Investors who enter the market during a speculative peak may find themselves holding an underwater position for years.

The Opportunity Cost of Zero Yield

Because gold is a “passive” asset, it produces no cash flow. It does not pay dividends or interest. In an environment where interest rates are high, the “opportunity cost” of holding gold becomes significant. An investor is essentially forgoing the yield of a savings account in the hope that gold’s price appreciation will outperform those lost earnings.

Storage, Insurance, and Hidden Costs

The logistics of physical ownership are both burdensome and expensive. Professional vaulting services and dedicated insurance premiums can slowly erode an investor’s gains. While tools like Eazy Insure simplify many types of coverage, specialized insurance for high-value precious metals often requires a bespoke approach.

Tax and Regulatory Complexity

In many regions, gold is categorized as a “collectible” for tax purposes. This often results in a higher capital gains tax rate than the rate applied to stocks. Additionally, large purchases or sales of physical bullion often require the filing of specific government forms.

Who It May Be Suitable For

Gold is generally most appropriate for conservative investors whose primary objective is the preservation of existing wealth. It serves well for those who already possess a diversified base of traditional assets and wish to add a layer of protection against systemic financial shocks. It is also favored by individuals with a long-term time horizon—typically a decade or more—which allows them to ignore the asset’s characteristic short-term price swings.

Who Should Be Cautious

Individuals seeking immediate income or short-term speculative profits should approach gold with extreme caution. Because it offers no yield, it is usually unsuitable for retirees who depend on their investment portfolios to cover monthly living expenses. Furthermore, investors with a low tolerance for price fluctuations may find the current volatility of the 2026 market to be psychologically taxing. Finally, gold should never be a substitute for a balanced retirement strategy; over-allocating to precious metals can lead to underperformance compared to the compounding growth of equity markets.

Alternatives and Related Options

For those interested in the themes of gold investing but who find the logistics unsuitable, there are several alternatives:

- Silver: Often moves in tandem with gold but tends to exhibit higher volatility and has a broader range of industrial applications.

- Gold Mining Equities: Investing in companies that find and extract the metal. These stocks can provide leverage to the gold price but carry operational risks.

- Inflation-Protected Securities (TIPS): These are government-backed bonds specifically designed to increase in value alongside inflation.

- Debt Consolidation Services: For those looking to free up capital to begin investing, services like TraceLoans debt consolidation can help manage existing liabilities to create a more stable financial foundation.

Frequently Asked Questions

1. What is a standard recommended allocation for gold?

Most advisors suggest a modest allocation, typically between 5% and 10% of a total portfolio. This allows the asset to provide diversification without significantly dragging down the portfolio’s overall growth potential.

2. Is it better to own physical gold or a gold-backed ETF?

This depends on the investor’s priorities. Physical gold offers total control but involves higher costs for storage. ETFs offer the convenience of being traded like a stock but involve management fees and do not give the investor actual possession of the metal.

3. Does the price of gold always rise during a recession?

Not necessarily. During the initial stages of a severe liquidity crisis, investors may sell their gold holdings to raise cash, which can cause the price to fall temporarily alongside the stock market.

4. How are gold prices actually set?

Gold prices are determined by a global network of buyers and sellers in the “over-the-counter” market and through futures contracts. The price reflects the intersection of mining supply and investor sentiment regarding inflation.

Conclusion

Gold continues to be a cornerstone of the global financial system, valued for its historical role as a reliable store of value and its unique physical properties. While it offers undeniable benefits as a hedge against inflation and a tool for diversification, it also presents challenges related to price volatility and the lack of periodic income. In the current economic landscape of 2026, gold remains a viable strategic ballast for many investors, provided it is treated as one element of a broad and disciplined investment strategy.