Gold has occupied a unique position in the global financial ecosystem for millennia, serving as both a medium of exchange and a definitive store of value. In 2026, the methods available to investors have matured significantly, moving far beyond the simple acquisition of jewelry or hidden coins. Today’s market offers a sophisticated spectrum of entry points, ranging from tangible bullion to high-tech digital fractions. For many, Gold Investment Strategies acts as a “financial insurance policy,” sought out during cycles of aggressive inflation, currency volatility, or global unrest. Because the price of gold often moves independently of traditional equities and fixed-income assets, it remains a primary tool for those looking to balance a portfolio against systemic shocks. Understanding the operational nuances of each investment vehicle is the first step toward making an informed allocation.

What Is Gold Investment?

At its core, Gold Investment is the Strategies commitment of capital into high-purity bullion for the purpose of wealth preservation or long-term growth. Unlike ornamental gold, which carries high markups for craftsmanship and design, investment-grade gold is valued strictly for its metal content. By 2026 standards, professional-grade gold must maintain a minimum purity of 99.5%, frequently referred to as 24-karat gold.

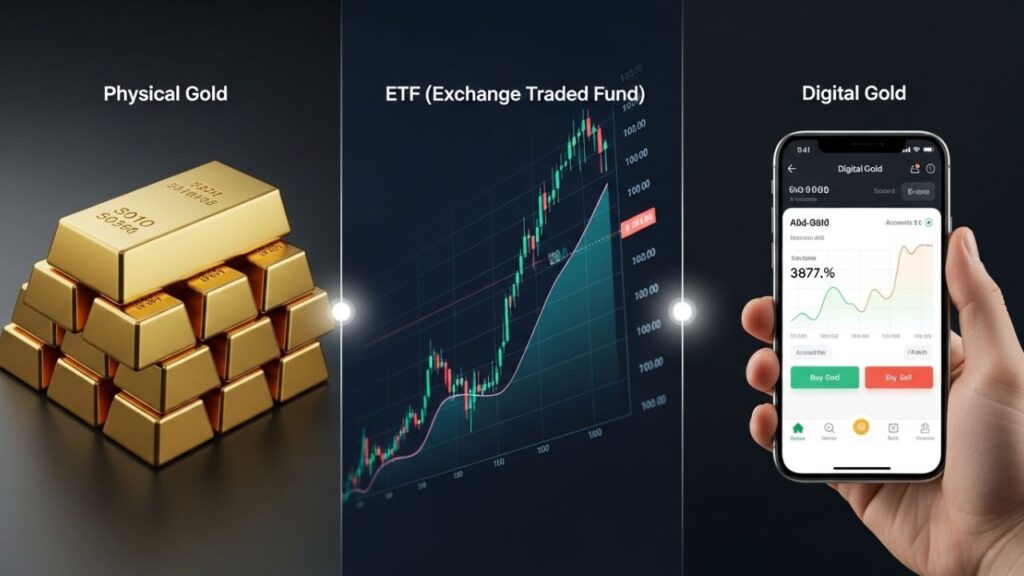

Modern investors typically navigate three distinct pathways to gain exposure:

- Physical Bullion: Direct ownership of tangible assets like bars or government-issued coins.

- Gold ETFs (Exchange-Traded Funds): Marketable securities that mirror the metal’s price, traded on major stock exchanges.

- Digital Gold: A contemporary fintech solution allowing for fractional ownership, where a provider buys and stores the metal in a professional vault on the user’s behalf.

How Gold Investment Works

The mechanics of “buying gold” depend entirely on which medium you choose. Each path carries its own set of logistical steps, from the initial transaction to the eventual liquidation of the asset.

1. Physical Gold

Acquiring physical metal is the most traditional route, placing the asset directly in the hands of the buyer.

- Sourcing: An investor identifies a reputable dealer or mint. They must choose between bullion bars—which offer lower premiums for bulk buys—and coins, which offer higher portability and legal tender status.

- The Transaction: The buyer pays the current “spot price” plus a dealer premium. This markup covers the costs of refining, minting, shipping, and the dealer’s profit margin.

- Custody: Once the metal is delivered, the responsibility for security shifts to the owner. This usually involves installing a high-grade home safe or leasing a private deposit box.

- Liquidation: Selling requires a physical appraisal. The owner must take the gold to a buyer who verifies its weight and purity before offering a “buy-back” rate, which is typically slightly lower than the current market spot price.

2. Gold ETFs

Exchange-Traded Funds act as a bridge, allowing investors to participate in the gold market through a standard brokerage account.

- Market Access: An investor uses their existing stock trading platform to search for specific gold fund tickers (such as GLD or IAU).

- Purchase: Shares are bought and sold just like company stocks. For investors who track Saul’s investing discussions, the focus is often on high-conviction growth, but gold ETFs provide a stabilizing counter-balance to that volatility.

- Backing: The fund manager is legally obligated to hold physical bullion in highly secure, audited bank vaults (often in London or New York) to back the value of every share issued.

- Price Tracking: The share price fluctuates in real-time throughout the trading day, staying tightly correlated with the international gold spot price.

3. Digital Gold

Digital gold is a modern hybrid, combining the fractional nature of an ETF with the ultimate goal of physical ownership.

- Account Creation: Through a mobile app or financial platform, an investor creates a digital wallet.

- Micro-Investing: Unlike physical bars, which require a significant upfront cost, platforms like GoMyFinance Invest allow users to buy gold for very small amounts, sometimes as little as a few cents.

- Insurance and Vaulting: For every gram purchased digitally, the provider places an equivalent physical amount in a secure, insured vault. The investor holds a digital certificate of ownership.

- Conversion: A unique feature of digital gold is the ability to eventually “convert” the digital balance into physical coins or bars for doorstep delivery once a certain weight threshold is reached.

Key Features and Core Components

Regardless of the format, several foundational pillars define the value and reliability of a gold investment.

- Purity and Hallmarking: Trust in gold is built on standardization. Investment-grade assets usually carry a hallmark or certificate of authenticity proving .999 or .9999 fineness.

- The Global Spot Price: This is the benchmark price for one Troy ounce of unrefined gold. It is determined by continuous trading on global commodities exchanges and serves as the baseline for all retail pricing.

- Counterparty Risk: This is a critical distinction. Physical gold held at home has no counterparty risk. Conversely, ETFs and digital platforms rely on the honesty of the provider. Understanding how a gating fund works is helpful here, as it illustrates how liquidity can sometimes be restricted in institutional settings.

- The “Spread”: In any gold transaction, there is a gap between the buying price and the selling price. High-volume ETFs usually have the narrowest spreads, while physical coins—due to their manufacturing and shipping costs—have the widest.

Benefits of Gold Investment

Gold remains a staple in diversified portfolios because it offers protections that paper or digital currencies cannot always guarantee.

- Resilience Against Inflation: When the cost of living rises and the purchasing power of the dollar shrinks, gold has a historical tendency to appreciate, acting as a “wealth stabilizer.”

- Universal Liquidity: Gold is perhaps the only asset that is recognized in every corner of the globe. It can be converted into any local currency with relative ease.

- Crisis Correlation: During periods of “market panic,” investors often sell stocks and move capital into gold. This “flight to safety” frequently causes gold to rise when the rest of a portfolio is falling.

- Tangible Value: Unlike a cryptocurrency or a company’s stock, gold has intrinsic physical properties and industrial uses that prevent its value from ever reaching zero.

Risks, Drawbacks, and Limitations

No investment is without its hurdles, and gold carries specific challenges that can erode returns if not managed properly.

- Ongoing Carrying Costs: Physical gold doesn’t just sit there; it must be protected. Insurance premiums and secure storage fees can act as a “negative yield” over time.

- The Opportunity Cost: One of the most significant drawbacks of gold is that it produces no cash flow. It does not pay dividends like a stock or interest like a bond. For those managing complex portfolios, including other comprehensive income items, gold’s lack of yield must be carefully balanced.

- Platform and Regulatory Risk: The digital gold sector is often less regulated than the stock market. If a digital provider lacks proper insurance or transparent auditing, the investor’s holdings could be at risk if the company fails.

- Transaction Friction: Buying a physical gold bar today and selling it tomorrow is almost always a losing trade. The combination of dealer markups, shipping, and taxes means the gold price must rise significantly just for the investor to break even.

- Price Volatility: While gold is a long-term stabilizer, its short-term price swings can be violent, often dictated by shifts in US interest rates or a strengthening dollar.

Who It May Be Suitable For

- Risk-Averse Savers: Those who are more concerned with “return of capital” than “return on capital” often find gold’s stability reassuring.

- Retirement Planners: Investors looking to protect the purchasing power of their nest egg over a multi-decade horizon.

- Hedgers: Sophisticated investors who want a specific counter-weight to a portfolio heavily weighted in high-risk technology stocks or emerging market currencies.

Who Should Be Cautious or Avoid It

- Active Traders: The costs associated with physical and digital gold make it inefficient for those looking to “day trade” or profit from hourly price moves.

- Growth-Focused Investors: Younger investors with a high risk tolerance may find that gold’s slow-and-steady nature hinders their ability to compound wealth as quickly as equities or venture capital.

- Liquidity-Dependent Households: If you might need to access your cash within a few weeks, the process of selling physical gold or waiting for fund settlements might be too slow and costly.

Alternatives or Related Options

If direct exposure to the metal isn’t the right fit, there are other ways to play the “precious metals” theme:

- Silver and Platinum: These metals share gold’s “safe haven” status but are more heavily tied to industrial production.

- Gold Mining Equities: Instead of owning the metal, you own the companies that dig it up. These stocks can provide higher returns when gold prices rise, but they also carry operational risks.

- Inflation-Linked Bonds: For those who only care about fighting inflation, government-backed inflation-indexed bonds provide a guaranteed real return.

Frequently Asked Questions

1. Is gold a better investment than the stock market?

“Better” is subjective. Over very long periods, the stock market has historically outperformed gold in terms of total return. However, gold often outperforms stocks during recessionary periods. Most experts view them as complementary rather than competitive.

2. How do I know if my gold is real?

When buying physical gold, always look for the weight, purity, and the stamp of a recognized refiner. Professional dealers use ultrasonic or X-ray fluorescence (XRF) testing to verify purity without damaging the metal.

3. What are the tax implications of selling gold?

In many jurisdictions, gold is treated as a “collectible” or a capital asset. This means you may owe capital gains tax on any profit you make when you sell. For those tracking institutional tools like a Term Finance Certificate, it is important to note that tax treatments vary significantly between corporate debt and physical commodities.

4. Can I put gold in my retirement account?

Yes, through a specialized “Gold IRA,” investors can hold physical bullion within a tax-advantaged framework. However, these accounts require a certified custodian and approved storage facilities; you cannot simply keep the gold at home.

Conclusion

The decision to invest in gold in 2026 involves balancing the desire for security with the need for efficiency. Physical gold remains the gold standard for those who value privacy and total independence from the financial system, though it requires a commitment to security. Gold ETFs offer the most seamless integration for the modern investor, providing high liquidity and professional oversight at a low cost. Digital gold provides a low-barrier entry point, ideal for those who wish to accumulate wealth incrementally. By understanding that gold is primarily a tool for wealth preservation rather than rapid speculation, an investor can choose the method that best safeguards their financial future.