Navigating the modern banking landscape requires more than just knowing your account balance; it demands an understanding of how financial institutions process the movement of money. Even for those who track their spending diligently, a “Non-Sufficient Funds” (NSF) event can occur. This happens when a payment request—whether a check, an automated bill pay, or a debit purchase—exceeds the liquid capital available in a bank account at that specific moment.

While an NSF notification is often viewed as a simple administrative hiccup, the reality is more complex. It initiates a series of automated responses from both your bank and the merchant you intended to pay. These responses can lead to immediate financial penalties and, if left unaddressed, may impact your ability to utilize standard banking services in the future. This article examines the mechanics of insufficient funds, the associated costs, and the practical steps consumers can take to maintain a healthy relationship with their financial institutions.

What Is Insufficient Funds (NSF)?

In the simplest terms, “insufficient funds” means the money currently accessible in your bank account is less than the amount you are trying to spend. This status is also known as Non-Sufficient Funds (NSF). When a bank receives a request for payment—such as a check you wrote or an electronic transfer for a utility bill—it checks your “available balance” to ensure the transaction can be covered.

If the account lacks the necessary funds, the bank has a choice: it can reject the payment entirely or, if you have certain protections in place, it can pay the amount anyway, which results in an “overdraft.” When the bank chooses to reject the transaction, the item is “returned unpaid” to the sender. This failure to complete the transaction is what triggers the specific status and the associated penalties known as NSF fees.

How It Works: The Process of a Failed Transaction

The journey of an NSF transaction involves several distinct stages within the banking system’s backend architecture. Understanding this timeline can help consumers intervene before fees compound.

- The Request for Payment: A merchant, service provider, or individual submits a payment request to your bank. This could be a physical check presented for deposit at another branch or an Electronic Funds Transfer (EFT).

- The Real-Time Balance Check: The bank’s software compares the requested amount against your “available balance.” It is important to note that this is different from your “total balance,” as it excludes pending deposits and funds held by merchants (like the temporary holds placed by gas stations or hotels).

- The Decision to Decline: If the available funds are inadequate, and no backup line of credit is linked to the account, the bank marks the transaction as “returned.” This is often referred to in traditional banking as a “bounced check.”

- The Assessment of Penalties: Once the transaction is rejected, the bank automatically assesses an NSF fee. This fee is meant to cover the administrative costs of processing a failed item. As of 2026, many credit unions and banks have adjusted these fees due to regulatory shifts, but they remain a standard consequence.

- Merchant Notification and Re-presentation: The party attempting to collect the money is notified that the payment was unsuccessful. Often, their automated systems will wait a few days and then attempt to process the payment again. If the account is still empty, a second NSF fee may be triggered.

Key Features of the NSF Experience

Several core components define what happens when an account falls short. Recognizing these terms is vital for clear communication with bank representatives.

- Bank-Side NSF Fees: These are the most immediate consequence. They are fixed-rate penalties charged per rejected item. If multiple subscriptions attempt to withdraw money on a day when the balance is zero, the account holder could be charged separate fees for each.

- Merchant-Side Penalties: The bank is not the only entity that charges for a failed payment. Most companies, from landlords to utility providers, have a “returned item fee” clause in their contracts.

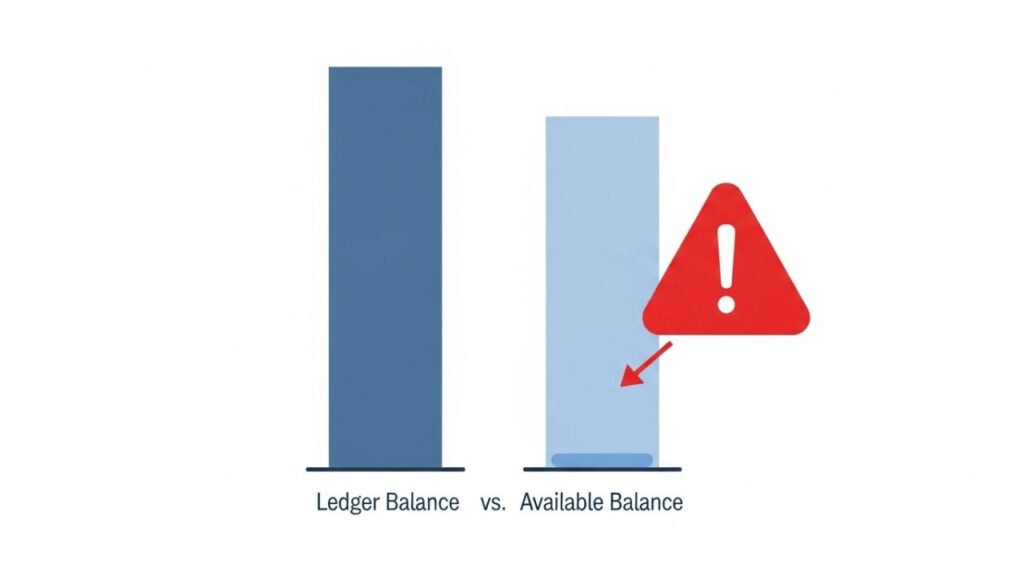

- Available vs. Ledger Balance: Your “ledger balance” is the total amount of money in the account. Your “available balance” is what you can actually spend. Transactions fail based on the available balance, which is why a payment can “bounce” even if you have a large deposit waiting to clear.

- The Negative Balance Cycle: Fees are deducted directly from the account. If your balance was $0 and you incur a $35 NSF fee, your balance becomes -$35. This negative standing can lead to further fees if not corrected immediately.

Benefits of Navigating NSF Protocols Correctly

While the situation itself is not inherently positive, there are realistic advantages to understanding how these protocols function. Being informed allows for a “damage control” approach that protects your financial standing.

- Leveraging Grace Periods: Some banks offer a “grace period” to deposit funds and avoid a fee. Knowing your bank’s specific cutoff time allows you to move money or deposit cash just in time to prevent a penalty.

- Maintaining Merchant Trust: By understanding the NSF process, you can contact a merchant as soon as a payment fails. Proactive communication often results in the merchant waiving their own late fees.

- Preserving Banking History: Consistently resolving NSF issues quickly shows the bank that the event was an anomaly rather than a pattern of mismanagement. This helps maintain your “good standing,” which is useful when applying for other services, such as a Term Finance Certificate or a new line of credit.

Risks, Drawbacks, and Honest Limitations

The impact of insufficient funds extends far beyond a single penalty. The risks are layered and can affect your financial mobility for years.

- The Domino Effect of Fees: When an account goes into the negative because of a fee, it becomes even easier for the next transaction to fail. For individuals living paycheck to paycheck, a single failed $10 transaction can lead to $100 in total fees if multiple items are presented while the account is negative.

- ChexSystems and TeleCheck Reporting: Banks report closed accounts with unpaid negative balances to specialized consumer agencies like ChexSystems. Most major banks screen applicants against these reports. A “black mark” here can prevent you from opening a basic checking account at almost any traditional bank for several years.

- Potential for Legal Complications: While rare for small amounts, intentionally writing checks with the knowledge that funds are insufficient is considered fraud in many jurisdictions.

- Impact on Future Credit: While the bank fee itself doesn’t lower your credit score, the missed payment to a creditor (like a car loan or credit card company) certainly will. A 30-day late payment can cause a significant drop in a FICO score.

Who This Information Is Suitable For

This educational overview is designed for a broad range of bank users, particularly those who want to transition from reactive to proactive financial management.

- Digital Banking Users: Individuals who rely heavily on “one-click” purchases or recurring app subscriptions that may be forgotten until they hit the account.

- Young Adults and Students: Those who are managing their own finances for the first time and may not realize that “pending” deposits aren’t immediately spendable.

- Individuals Managing Debt: Understanding balance timing is crucial for those paying down obligations, such as inheriting a house with debt, where large payments must be timed precisely.

Who Should Be Cautious

Certain groups should exercise extra care, as the margin for error in their accounts may be smaller or the stakes of an NSF event higher.

- Low-Balance Account Holders: If your average daily balance is close to zero, the risk of a “hidden” subscription or an unexpected service fee triggering an NSF event is significantly higher.

- Joint Account Holders: When two people spend from the same pool of money without real-time communication, it is very easy to overspend. Both parties are equally responsible for any fees incurred.

- Small Business Owners: Business accounts often have different fee structures. Multiple NSF events can lead to a bank freezing a business line of credit or affecting their standing in an Organised Trading Facility.

Alternatives and Related Options

Preventing an NSF event is generally more cost-effective than dealing with the aftermath. Several standard banking tools can serve as a safety net.

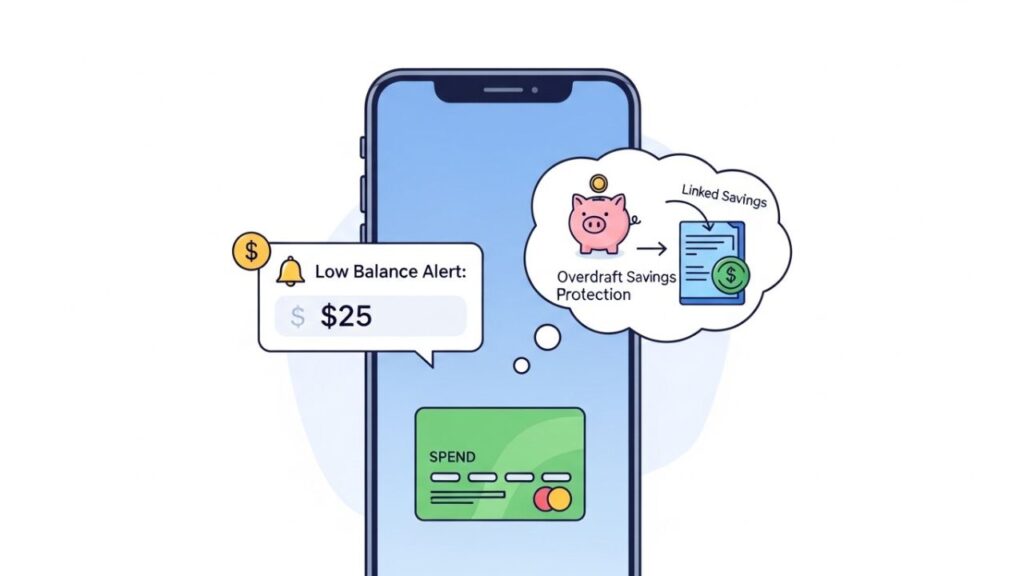

- Overdraft Protection Linkage: You can link your checking account to a savings account. If you overspend, the bank pulls the exact amount needed from the backup source. While there may be a small transfer fee, it is usually a fraction of an NSF fee.

- Low-Balance Mobile Alerts: Most modern banking apps allow you to set a “floor” for your account. If your balance drops below $50, for example, the bank sends an immediate notification, giving you time to stop spending.

- Using Specific Credit Tools: For some, using a dedicated card for small purchases, such as those found via ziimp.com credit cards, can help keep daily spending separate from the primary checking account where bills are paid.

Frequently Asked Questions (FAQ)

1. How long does it take for an NSF fee to appear?

In most cases, the fee is assessed and deducted from your balance the same business day the transaction is rejected. Some banks batch these fees and apply them overnight.

2. What is ADTQ in my bank account?

If you see unfamiliar codes on your statement after a failed transaction, it is important to understand what they represent. You can learn more about what is ADTQ in my bank account to better decode your transaction history.

3. Why was I charged a fee when my balance showed I had money?

This is usually due to the difference between your “actual” and “available” balance. If you deposited a $1,000 check yesterday, the bank may hold a portion of it for several days. Even though your total balance says $1,000, you only have a smaller amount available to spend.

4. Will the bank close my account after one NSF event?

Typically, not a single NSF will shut down an account. However, negative balances or recurring NSFs can result in closure and ChexSystems reporting.

5. Are NSF fees the same at every bank?

Fees vary by bank and state. Internet banks can forego NSF charges. The standard banks will charge between 10 and 35 dollars per transaction.

Conclusion

Bank account management is not limited to the monitoring of deposits. It involves the awareness of the regulations of the failed transactions. An insufficient funds occurrence is a situation where outgoings surpass money. The charges can be annoying, however they serve as a reminder. These problems can be prevented with the help of alerts, account linkages, and automatic transfers. On its part, every bank has its own policies and therefore it is important to know them. Maintaining a low balance in your account takes care of unforeseen expenses. Being a curious and active person will help you evade charges and keep your money sound. It is always good to plan in advance and keep your account healthy and stable.