The architecture of European financial markets saw a fundamental shift with the implementation of the Markets in Financial Instruments Directive II (MiFID II). Among the most significant developments within this regulatory overhaul was the birth of the Organised Trading Facility, or OTF. This venue was specifically engineered to bring a new level of transparency to corners of the market that had historically operated in the shadows—the “dark” pools of liquidity where high-stakes trades often occurred without public oversight.

By establishing a formal framework for trading non-equity instruments, the OTF effectively bridges the gap between rigid traditional exchanges and the informal, bilateral world of over-the-counter (OTC) agreements. For anyone navigating the professional financial landscape, grasping the role of the OTF is vital. It represents a move toward standardized reporting and heightened supervision in the trading of bonds, derivatives, and other complex assets. This article examines how these facilities function, why they exist, and how they fit into the broader global economy.

What Is an Organised Trading Facility (OTF)?

At its core, an Organised Trading Facility is a regulated platform designed to let multiple third parties buy and sell specific financial products. However, unlike the New York Stock Exchange or Euronext, an OTF does not handle company shares. Instead, it is legally restricted to non-equity instruments. These include corporate and government bonds, structured finance products, emission allowances, and a wide array of derivatives.

The OTF was introduced to capture trading activity that previously happened via inter-dealer brokers or through private phone calls and chat rooms. What truly sets an OTF apart from other venues is the concept of discretion. On a standard stock exchange, trades are matched automatically by a computer based on strict rules. In an OTF, the person or entity running the platform can use their own judgment to decide how to pair buyers and sellers to get the most favorable outcome for everyone involved.

How an OTF Works: Step-by-Step

The journey of a trade within an OTF is more nuanced than a typical retail stock purchase. It involves a sophisticated interplay between technology and human oversight.

- Client Enrollment: Unlike public exchanges where traders are often called “members,” those using an OTF are classified as “clients.” This nomenclature is significant because it triggers specific legal protections.

- Submitting an Interest: A client—usually a large bank or hedge fund—will signal their intent to trade a specific instrument, such as a high-yield corporate bond or a complex interest rate swap.

- The Discretionary Matching Process: The operator scans the available interests within the system. Instead of relying solely on an algorithm, they might use professional judgment to facilitate a match.

- Executing the Trade: Once a suitable counterparty is found, the transaction is finalized. In certain regulated scenarios, the operator might act as a “matched principal,” briefly stepping into the middle of the trade.

- Transparent Reporting: Once the trade is complete, the OTF must report the price and size to regulators and the public. This ensures that even niche trades contribute to overall market transparency.

Strategic Liquidity and Market Context

In the broader context of asset management, understanding where a fund executes its trades is just as important as the assets it holds. However, if that same manager needs to hedge currency risk using complex derivatives, they might move that specific portion of their activity to an Organised Trading Facility to take advantage of discretionary matching.

Key Features and Core Components

To truly understand an OTF, one must look at the specific pillars that support its regulatory definition:

- Specific Asset Focus: OTFs are “non-equity” only. They are the primary domain for debt instruments and environmental credits.

- Operator Judgment: The OTF is the only multilateral venue where the operator can legally intervene and use their discretion to manage the flow of trades.

- A Protected Client Base: Because participants are clients, the operator has a fiduciary-like responsibility, including “Best Execution” obligations.

- Multilateral Interaction: Despite the operator’s ability to intervene, the system must allow multiple third-party interests to interact.

Benefits and Advantages

The shift toward OTFs has brought several tangible improvements to how global finance operates:

- Price Discovery: By centralizing activity on a regulated platform, the industry gains a much clearer picture of what niche assets are actually worth.

- Tailored Execution: Large institutional orders can be “market-sensitive.” The discretionary nature of an OTF allows for a “high-touch” approach to minimize price disruption.

- Reduced Systemic Risk: Organizations like the Financial Conduct Authority (FCA) and the European Securities and Markets Authority (ESMA) monitor these trades, which reduces hidden risk in the financial system.

- Operational Integrity: The compliance standards for running an OTF ensure the venue follows strict anti-money laundering and market abuse protocols.

Financial Resilience and Trading Venues

When financial institutions face internal hurdles, such as a liquidity crunch or an insufficient funds scenario at a clearing level, the regulated nature of an OTF provides a safety net. Because every trade is reported and monitored, it is much harder for systemic failures to go unnoticed. This level of oversight is a far cry from the pre-2018 era, where large OTC bond trades could happen in a vacuum, potentially hiding significant capital weaknesses from the broader market.

Risks, Drawbacks, and Limitations

No financial structure is without its downsides. It is important to look at OTFs with a critical eye:

- The “Human” Factor: Discretion introduces the risk of human error or subjective bias. A client might prefer the unbiased nature of a pure algorithm.

- High Barrier to Entry: Setting up an OTF is expensive due to the heavy regulatory burden, and these costs are often passed down to clients.

- Segmented Liquidity: Fragmented venues mean a buyer might be on one platform while the perfect seller is on another.

- Potential for Conflicts: There is a lingering concern that an operator might favor certain clients when exercising discretion, requiring constant, vigilant auditing.

Who It May Be Suitable For

The OTF is a professional tool built for a professional audience. It is most effective for:

- Institutional Fund Managers: Those managing pension funds who need to move large amounts of capital without causing a stir in the markets.

- Corporate Treasurers: Companies looking to trade derivatives to hedge against interest rate or currency fluctuations.

- Government Agencies: Entities involved in the sale of sovereign debt or the trading of carbon emission allowances.

Institutional Investing Discussions

For those deeply involved in high-level market analysis, participating in Sauls investing discussions can provide insight into how professional traders view these venues. These discussions often highlight the transition from traditional OTC trading to the more transparent OTF model. While the technical details of an organised trading facility might seem dense, the practical impact on how large-scale portfolios are balanced is a frequent topic among those navigating MiFID II regulations.

Who Should Be Cautious or Avoid It

This environment is not a “one size fits all” solution. Certain groups should look elsewhere:

- Individual Retail Traders: Most retail investors will never interact with an OTF. The products traded there are often too complex for non-professional accounts.

- Equity Enthusiasts: If your primary interest is the stock market, you are better served by Regulated Markets (Exchanges) or Multilateral Trading Facilities.

- Small-Scale Speculators: High costs and institutional requirements make these platforms inefficient for small, frequent trades.

Alternative Investment Instruments

While an OTF handles the trading of existing debt, the instruments themselves vary in structure. For instance, a term finance certificate is a specific type of debt instrument that might be traded within such a facility or through other specialized venues. Understanding the difference between the “venue” (the OTF) and the “instrument” (the certificate) is a key step in financial literacy for those moving beyond basic stock trading into the world of fixed income and structured finance.

Alternatives or Related Options

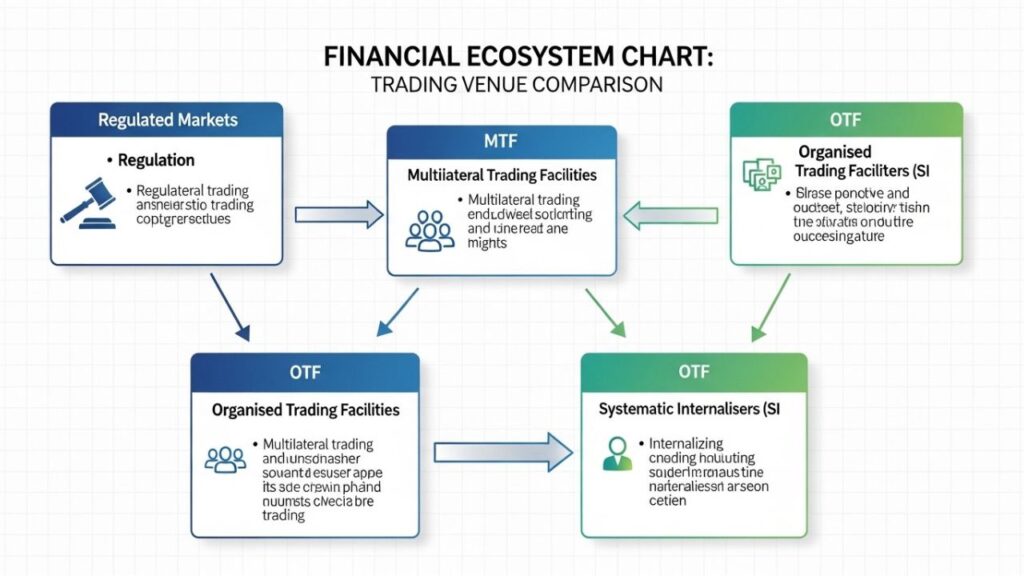

If an OTF doesn’t fit a firm’s needs, they generally turn to one of three other structures:

- Regulated Markets (RM): These are the gold standard of exchanges, primarily used for blue-chip stocks.

- Multilateral Trading Facilities (MTF): Similar to OTFs but without the “discretion” component. They are strictly rules-based.

- Systematic Internalisers (SI): Large investment banks that trade directly with their clients from their own inventory.

Frequently Asked Questions (FAQs)

1. Is an OTF the same as a “Dark Pool”? Not exactly. While some “dark” trading can occur within an OTF, the facility itself is a regulated, transparent venue that must report its trades to the public.

2. Why was the OTF created only for non-equities? Regulators felt the equity market was already well-served by existing exchanges. The non-equity market, however, lacked a formal, transparent structure for “high-touch” trading.

3. Does the operator of an OTF take the other side of my trade? Usually, no. They act as a facilitator. However, in specific cases, they can engage in “matched principal” trading to bridge the gap between two clients.

4. How can I tell if a platform is an OTF? All regulated venues must disclose their status in their legal documentation. You can also verify their status via the public registers maintained by the FCA or ESMA.

Conclusion

The Organised Trading Facility is a vital, if complex, piece of the global financial puzzle. It provides a structured environment for the trading of non-equity assets, bringing much-needed clarity to the world of bonds and derivatives. By combining the flexibility of human discretion with the safety of heavy regulation, the OTF ensures that institutional trading remains efficient and transparent. While it may not be a household name for the average investor, its role in maintaining a stable and fair financial ecosystem is fundamental to modern market integrity.