In the world of corporate finance, the “bottom line” is often treated as the ultimate indicator of success. However, Net Income—the traditional measure of profit—does not always tell the entire story of a company’s financial health. To capture a more complete picture, accountants use a category known as Other Comprehensive Income (OCI). This metric tracks specific financial fluctuations that, while significant, have not yet resulted in a completed cash transaction.

By separating these items from standard operational earnings, OCI provides a transparent view of how external market forces impact a firm’s total value. Understanding OCI is essential because it bridges the gap between a company’s daily business activities and its long-term economic standing. For example, if a multinational corporation holds significant assets in a foreign currency, the value of those assets will shift daily. Recording these shifts as immediate profit or loss would create immense volatility. OCI acts as a “holding pen” for these values, ensuring they are acknowledged without distorting the narrative of core profitability.

What Is Other Comprehensive Income?

Other Comprehensive Income (OCI) includes revenues, expenses, gains, and losses that accounting rules require companies to exclude from Net Income. This means the company has not yet sold the asset or settled the liability to turn the gain or loss into actual cash.

In simpler terms, OCI is where accountants record “paper” gains and losses. OCI affects the company’s total equity but stays separate from earnings generated by selling products or providing services. This is a critical concept for those looking to understand other comprehensive income and its role in a balanced financial report.

How It Works: The Accounting Process

The journey of an OCI item from a market fluctuation to a finalized entry on a financial statement follows a structured, multi-step logical path.

- The Trigger Event: A company identifies a change in the fair market value of a specific asset or liability, such as a shift in the price of a corporate bond or a change in a future pension payout.

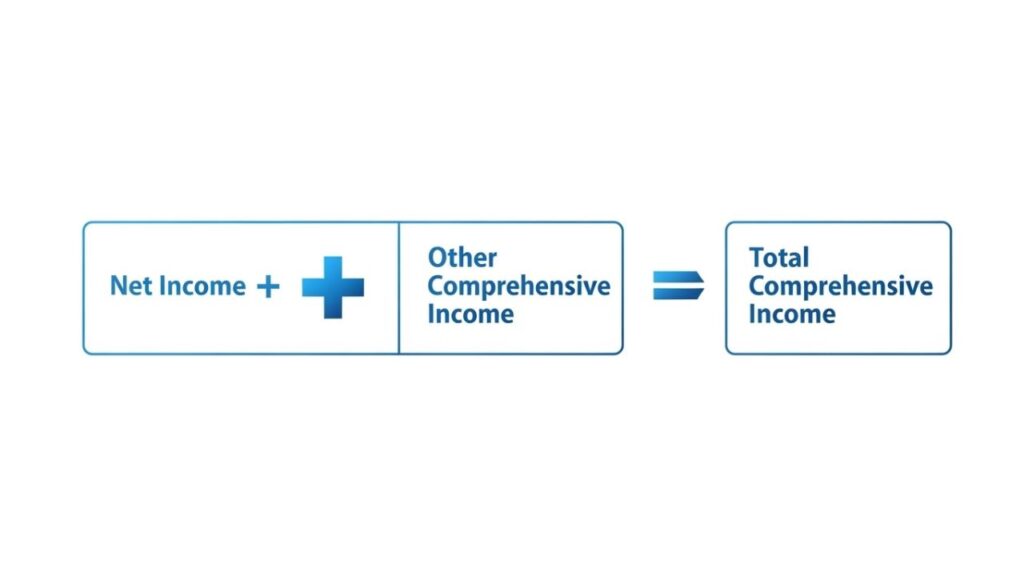

- Initial Recording: Instead of placing this value on the standard Income Statement, the accountant records it in the Statement of Comprehensive Income. This document starts with Net Income and then adjusts for OCI items to reach “Total Comprehensive Income.”

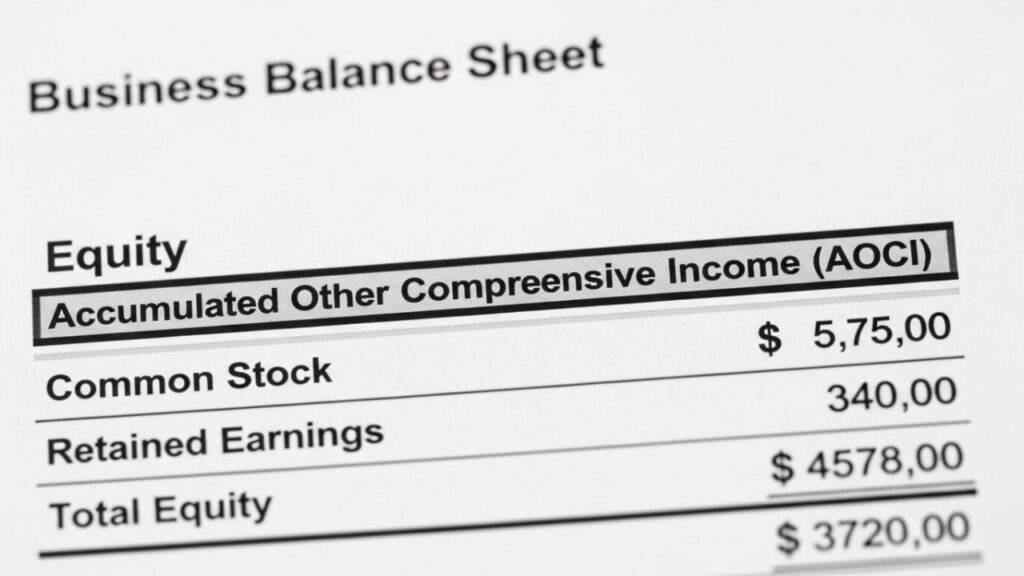

- Accumulation on the Balance Sheet: By the end of the period, the company takes OCI and charges it to the equity part of the balance sheet and accounts it in a statement termed Accumulated Other Comprehensive Income (AOCI) account.

- The Realization (Recycling): The paper gain or loss is realized when the company sells the asset or settles the liability. The company then transfers it through AOCI to Net Income and identifies it as a conclusive profit or loss.

Key Components of OCI (The FUPIE Framework)

To help professionals remember which items qualify for this treatment, the industry often uses the acronym FUPIE:

- Foreign Currency Translation: Adjusting the books of foreign subsidiaries back into the parent company’s currency.

- Unrealized Gains and Losses: Such a problem is also common in available-to-sale debt securities because the market price fluctuates but the company has not sold the bond.

- Pension Plan Adjustments: Gains or losses resulting from changes in the valuation of future retiree obligations.

- Instrument-Specific Credit Risk: Changes in the value of a company’s own debt based on its creditworthiness.

- Effective Cash Flow Hedges: The portion of a derivative’s value change used to protect against future price swings (like fuel costs).

Benefits and Advantages of OCI

- Improved Earnings Stability: By isolating market volatility, OCI allows companies to report a Net Income figure that reflects actual operational efficiency.

- Enhanced Predictive Value: When analysts see OCI items separately, they can better predict future cash flows once the company realizes those gains or losses.

- Asset-Liability Management: It provides a clear view of how well a company is managing risks, such as currency fluctuations or interest rate changes.

- Comprehensive Transparency: It ensures the company does not hide major valuation changes off the balance sheet and gives shareholders full disclosure.

Risks, Drawbacks, and Limitations

- Significant Complexity: OCI is one of the most difficult areas of accounting, often requiring sophisticated models to determine “fair value.”

- Impact on Financial Ratios: Because OCI affects the Equity section of the balance sheet, it can impact a company’s debt-to-equity ratio, even if operations are healthy.

- The “Recycling” Confusion: Transferring items that were in OCI to Net Income can mislead the investors and could give the impression that the company has realized the same gain twice.

- Opaque Valuation Methods: Many OCI items rely on management’s assumptions and estimates, which can be prone to error compared to realized cash transactions.

Who It May Be Suitable For

The detailed analysis of OCI is most useful for individuals who need a structural understanding of a company’s financial position. This includes Equity Analysts looking for the “quality” of earnings and Institutional Investors assessing long-term solvency. It is also vital for Corporate Lenders who need to see the total equity cushion protecting their loans.

Who Should Be Cautious

Retail Investors should be careful not to mistake a high OCI gain for actual cash that can be used for dividends. Furthermore, those focusing on daily price movements may find OCI less relevant than Net Income. If you see an unfamiliar code like ADTQ in your bank account, it is usually an internal banking code unrelated to these broad corporate accounting categories.

Alternatives and Related Options

If OCI seems too volatile for your analysis, consider these related financial metrics:

- Free Cash Flow (FCF): Focuses strictly on the actual cash generated, ignoring “paper” valuation changes.

- EBITDA: Strips out non-operational costs to see the core profitability of the business.

- Statement of Cash Flows: Provides a direct look at how much liquidity is actually moving through the business, which is useful when dealing with insufficient funds or liquidity issues.

Frequently Asked Questions

Can a company have negative OCI but positive Net Income? Yes. A company might be profitable in its operations but see the market value of its foreign investments or bond holdings drop due to external economic factors.

Is OCI the same as profit? No. Profit usually refers to “realized” gains. OCI consists of “unrealized” gains that haven’t been converted to cash yet.

Does OCI affect taxes? Generally, taxes are paid only when a gain is realized. However, companies must record the potential future tax impact of OCI items on their balance sheet.

Where is OCI located on a financial statement? The company records it in the Statement of Comprehensive Income and accumulates it in the equity of the balance sheet as Accumulated Other Comprehensive Income (AOCI).

Conclusion

Other Comprehensive Income is a vital bridge between operational performance and total market valuation. By categorizing unrealized gains and losses separately, it provides a more nuanced reflection of a company’s financial reality. Whether you are analyzing PayPal stock or a multinational bank, understanding OCI is essential for a complete view of long-term stability.