The landscape of global finance has undergone a radical transformation over the last two decades, with paypal stock Holdings Inc. (PYPL) serving as a primary architect of the digital payments revolution. As a staple of the NASDAQ exchange, PayPal represents one of the world’s most recognized standalone payment platforms. For investors, understanding this stock requires looking beyond a simple ticker symbol; it involves analyzing how a fintech pioneer maintains its relevance in an ecosystem now crowded with digital wallets, “buy-now-pay-later” services, and deep banking integrations.

Investing in PayPal is essentially a stake in the continued digitization of commerce. However, as the company matures, its role has shifted from a high-growth disruptor to a value-oriented financial giant. This article explores the mechanics of the PayPal business model, its core components, and the specific risks that investors must weigh when considering the stock for a diversified portfolio.

What Is PayPal Holdings Inc. (PYPL)?

PayPal Holdings Inc. is a technology company that facilitates a global digital payments platform, allowing consumers and merchants to transfer money securely. Originally founded in the late 1990s and later spun off from eBay in 2015, the company has grown into a multi-brand powerhouse. Its umbrella includes not only the signature PayPal button but also Venmo, Braintree, and the shopping tool Honey.

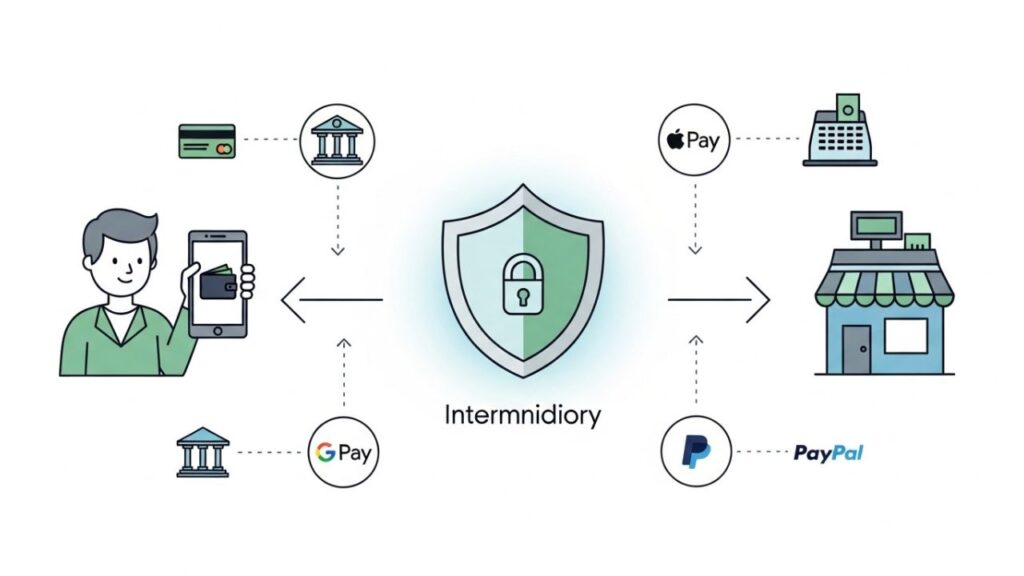

At its core, PayPal acts as a secure intermediary. It creates a digital layer between a user’s sensitive banking information and the merchant. By “vaulting” this data, it allows shoppers to make purchases without sharing credit card details with every individual retailer. For shareholders, the stock represents equity in this massive infrastructure and the transaction fees generated by its hundreds of millions of active accounts.

How the PayPal Business Model Works

PayPal’s revenue is largely driven by volume. The company operates a “two-sided network,” meaning it provides essential services to both the person spending the money and the entity receiving it. Here is the step-by-step flow of how the business generates income:

- Account Integration: Users link their credit cards, debit cards, or bank accounts to a PayPal or Venmo digital wallet.

- Facilitating the Transaction: When a consumer hits “buy” or sends money to a friend, PayPal manages the movement of those funds across the digital landscape.

- Fee Collection: While peer-to-peer transfers are often free, PayPal charges merchants a percentage of the sale plus a small fixed fee for every transaction processed through its gateway.

- Value-Added Services: Beyond basic fees, the company earns interest on funds held in user balances, charges for currency conversion on international trades, and collects interest from credit products.

- Settlement: PayPal clears the transaction and deposits the funds into the merchant’s account, typically bypassing the longer wait times associated with traditional bank wires.

Key Features and Core Components

The company’s market position is built on several distinct pillars that serve different segments of the economy:

- Branded Checkout: This is the iconic “PayPal” button found on millions of websites. It remains the company’s most profitable product due to its high level of consumer trust.

- Venmo: A mobile-first social payments app dominant in the United States. While it started as a way to “split the bill,” it now offers debit cards and merchant payment options.

- Braintree: This is “unbranded” technology used by large enterprises like Uber or Airbnb. It handles the backend payment processing without the consumer ever seeing a PayPal logo.

- PayPal Honey: A browser extension that helps consumers find coupons and rewards. This tool integrates PayPal earlier in the shopping process, before a user even reaches the checkout page.

- Credit and BNPL: PayPal offers “Buy Now, Pay Later” installments, allowing it to capture a share of the consumer lending market while increasing transaction sizes for merchants.

Benefits and Advantages

Investors are often drawn to PayPal because of its massive scale and established “moat.” A primary advantage is Brand Authority. In an era of frequent data breaches, many shoppers prefer using a known entity like PayPal rather than entering financial details into an unfamiliar website.

Additionally, the company thrives on Network Effects. As more merchants accept PayPal, the service becomes more indispensable to consumers; as the user base grows, merchants feel more pressure to offer it. Finally, PayPal’s Data Sophistication is a significant asset. By seeing both sides of a transaction, the company can refine its fraud prevention algorithms and develop highly targeted financial products that competitors might struggle to replicate.

Risks, Drawbacks, and Limitations

No investment is without hurdles, and PayPal faces several challenges that have impacted its market valuation.

1. Intense Competition: The payments space is no longer a one-horse race. PayPal faces mounting pressure from “Big Tech” (Apple Pay and Google Pay), traditional card networks like Visa, and newer fintech rivals such as Stripe and Adyen. Apple Pay, in particular, is a formidable threat due to its seamless integration into the iPhone’s hardware.

2. Margin Compression: While the total amount of money processed by PayPal (Total Payment Volume) continues to rise, much of that growth comes from unbranded services like Braintree. These services are less profitable than the “branded” PayPal button, which can lead to shrinking profit margins even as the company grows larger.

3. Economic Sensitivity: PayPal’s health is tied directly to consumer spending. During periods of high inflation or recession, people buy fewer non-essential goods. This drop in discretionary spending hits PayPal’s transaction revenue almost immediately.

4. Technological Inertia: As a pioneer, PayPal deals with “legacy” systems. It must constantly innovate to keep up with leaner, cloud-native startups while ensuring its massive, older infrastructure remains secure and functional.

Who This Investment May Be Suitable For

PayPal might be a fit for investors seeking exposure to Fintech and E-commerce who prefer an established leader over a speculative startup. It often appeals to Value Investors who believe the company’s current stock price is low relative to the significant cash it generates. Because it is a mature tech company, it may also attract those looking for a “defensive” technology play—one with a proven track record rather than unproven promises.

Who Should Be Cautious or Avoid It

Investors chasing Aggressive, High-Speed Growth may find PayPal disappointing, as its days of explosive, triple-digit gains have largely passed. Those wary of Platform Risk—the danger of being boxed out by companies that own the operating systems (like Apple or Google)—might also hesitate. Finally, if you cannot tolerate the volatility common in the tech sector, the sharp swings in PayPal’s share price might not align with your risk tolerance.

Alternatives and Related Options

If the payments sector interests you but PayPal does not, consider these alternatives:

- Payment Rails: Visa (V) and Mastercard (MA) provide the fundamental infrastructure for digital commerce.

- Direct Rivals: Block Inc. (SQ), the parent of Cash App and Square, offers a different approach to the digital wallet.

- E-commerce Giants: Amazon (AMZN) or Shopify (SHOP) benefit from the same digital shopping trends but through different business models.

- Fintech ETFs: Funds like the Ark Fintech Innovation ETF (ARKF) offer a “basket” of various fintech stocks, reducing the risk of betting on a single company.

Key Points on Market Integration and Consumer Impact

As PayPal continues to evolve, its impact on broader consumer financial behaviors and its place within the regulatory landscape remain pivotal.

- Platform Diversification: PayPal’s move into broader financial tools highlights a shift toward becoming a “one-stop shop” for digital finance.

- Digital Transformation: The company drives the adoption of paperless systems, much like the WebWise Banking initiatives seen in traditional sectors.

- Credit Accessibility: By offering BNPL and credit lines, PayPal competes directly with regional lenders like HomeBank Quincy IL.

- Convenience and Security: PayPal’s value proposition relies on ease of use, a priority shared by specialized payment portals like PayMyENTBill or PayMyDoctor.

Frequently Asked Questions

1. Does PayPal pay a dividend?

Historically, the company focused on reinvesting profits or buying back shares. However, as of early 2026, PayPal has introduced a modest quarterly dividend, marking its transition into a more mature “capital return” phase.

2. How does Venmo make money if peer-to-peer transfers are free?

Venmo earns revenue through “Instant Transfers” (where users pay a fee to move money to their bank immediately), interchange fees from its branded debit cards, and fees paid by businesses that accept Venmo at checkout.

3. Is PayPal considered a bank?

No. PayPal is a financial technology company and a licensed money transmitter. While it offers features like savings accounts and debit cards, these are typically provided through partnerships with FDIC-insured banks.

4. Why is the “PayPal Button” so important?

The branded button is PayPal’s “high-margin” product. Because it carries the PayPal name and provides a high level of security and convenience, the company can charge merchants higher fees for it compared to basic backend processing.

Conclusion

PayPal Holdings Inc. remains a cornerstone of the digital economy, defined by a massive user base and a versatile suite of tools. Its shift from a high-growth “disruptor” to a mature, value-centric entity reflects the natural evolution of the fintech industry. While the company must navigate fierce competition and shifting profit margins, its ability to generate significant cash flow remains a key characteristic. As with any investment, potential shareholders should weigh PayPal’s historical dominance against the rapid technological changes currently reshaping how the world moves money.