In the intricate world of corporate finance, companies frequently find themselves at a crossroads when they need to fund large-scale ambitions. Whether the goal is to break ground on a new manufacturing facility, modernize aging infrastructure, or restructure existing debt, the capital required often exceeds what a standard bank loan can provide. While many people are familiar with “going public” by issuing stocks, there is another, equally vital path for raising capital: the debt market. Within this space, Term Finance Certificates (TFCs) serve as a primary vehicle for corporations to secure medium- to long-term funding directly from the investing public.

A TFC functions as a sophisticated bridge between a corporation’s need for stable liquidity and an investor’s desire for a predictable income stream. Especially prevalent in developing financial markets, these certificates are more than just financial jargon; they are essential instruments that drive industrial growth and provide a structured alternative to equity volatility. By understanding how TFCs operate, individuals can gain a clearer picture of how corporate debt functions as a cornerstone of a diversified financial strategy.

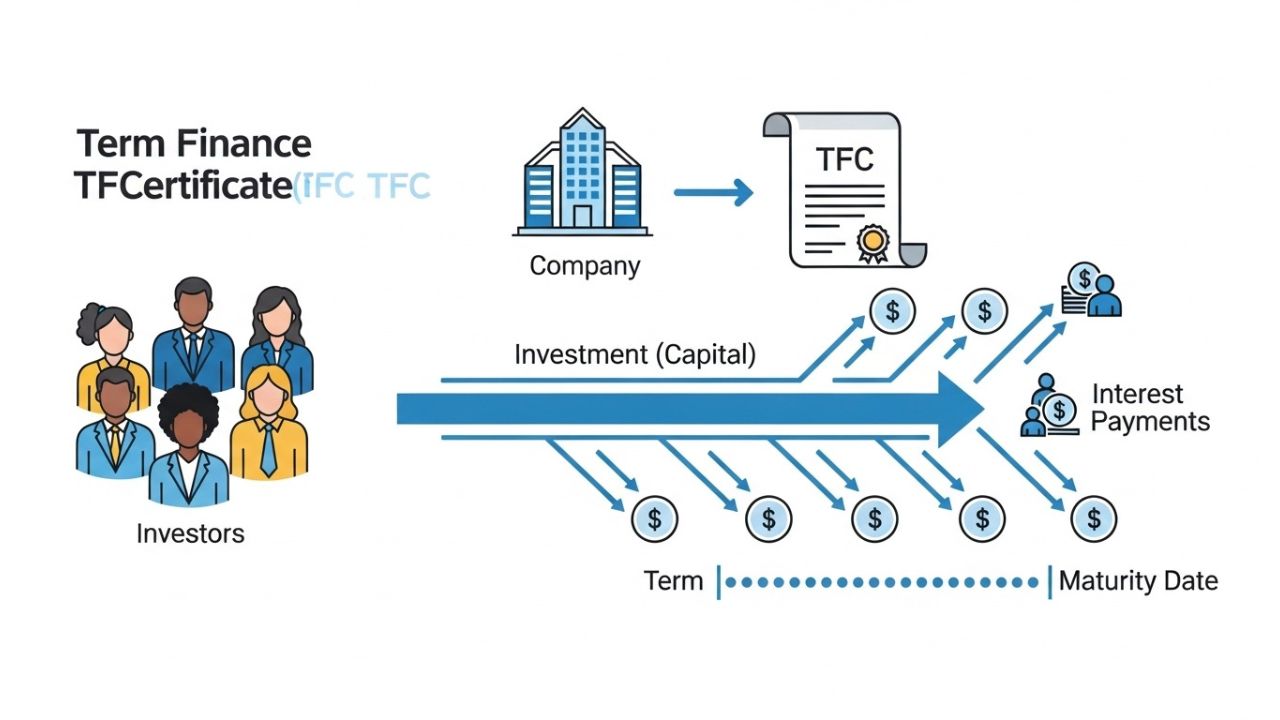

Term Finance Certificate?

At its most fundamental level, a Term Finance Certificate (TFC) is a formal “IOU” issued by a corporation. It is a debt instrument that allows a company to borrow money from investors for a specific duration. Unlike a stock, which grants you a piece of ownership and a say in company decisions, a TFC is a contract of debt. When you purchase one, you are acting as a lender to whom the company owes a specific obligation.

These certificates represent “redeemable capital,” a term signifying that the money borrowed must be paid back by a certain date. They are typically issued by established entities, such as large manufacturing firms or commercial banks, to raise funds without diluting the ownership of existing shareholders. Because most TFCs are listed on a stock exchange, they possess a level of transparency and tradability that private loans lack, making them an accessible entry point for those looking to explore the corporate bond market.

How It Works

The lifecycle of a TFC is a structured process that ensures both the company and the investor understand their obligations from the outset. The procedural steps are relatively straightforward:

- The Planning Phase: The corporation identifies a funding gap and determines how much it needs to borrow, for how long, and what interest rate it can afford. This information is compiled into a prospectus.

- Subscription: Investors review the terms and decide to buy into the debt. Once the subscription period ends and the target amount is met, the company issues the certificates.

- Utilization of Funds: The capital raised is deployed into the company’s operations. However, if a company manages its cash poorly and experiences insufficient funds, it may struggle to meet the obligations of the TFC.

- The Coupon Period: Throughout the life of the TFC, the company makes regular interest payments, known as “coupons.” These might arrive in your account every quarter, every six months, or once a year.

- Ongoing Surveillance: Credit rating agencies continuously monitor the company. If the company’s financial health improves, its rating might go up; if it struggles, the rating may drop.

- Redemption and Maturity: When the term ends, the company pays back the original principal. In some cases, this repayment happens in installments over the last few years of the certificate’s life.

Key Features of TFCs

To distinguish a TFC from other types of investments, it helps to look at the specific characteristics that define its structure:

- The Maturity Date: Every TFC has an expiration date. This tenure usually lasts between three and ten years, making it a medium-to-long-term commitment.

- The Coupon Mechanism: The interest rate can be fixed (staying the same throughout) or floating (benchmarked against a market rate).

- Security Interests: Many TFCs are “secured” by specific assets of the company, such as land or equipment. This provides a safety net if the company defaults.

- Credit Quality: Before a TFC is offered, it is graded by a credit rating agency. These ratings act as a shorthand for the company’s ability to keep its promises.

- Marketability: Because these certificates are usually listed on a stock exchange or an organised trading facility, you aren’t necessarily locked in until maturity. You can sell your TFC to another investor through a broker.

Benefits and Advantages

For an investor seeking alternatives to the stock market, TFCs offer a balanced middle ground:

- Consistent Cash Flow: One of the most attractive qualities of a TFC is the regularity of coupon payments. This predictability is invaluable for those who rely on investments for supplemental income.

- Competitive Returns: Corporations usually offer higher interest rates than banks to attract lenders. This “risk premium” means TFCs often outperform traditional fixed-income products.

- A Shield Against Volatility: When the stock market crashes, the debt markets often remain more stable. Including TFCs in a portfolio can act as a stabilizer.

- Legal Protections: As a debt holder, you have a stronger legal standing than a shareholder. If a company faces liquidation, creditors and debt holders are prioritized for payout.

Risks, Drawbacks, and Limitations

No investment is without its pitfalls, and corporate debt carries specific risks that require a cautious approach:

- Credit or Default Risk: The company may face a liquidity crisis and stop paying interest. Even a “secured” TFC doesn’t guarantee a 100% recovery if the collateral loses value.

- Interest Rate Fluctuations: There is an inverse relationship between interest rates and bond prices. If market rates rise, your existing fixed-rate TFC becomes less valuable.

- The Liquidity Trap: Just because a TFC is listed doesn’t mean there is always a buyer. In times of economic uncertainty, the secondary market can “dry up.”

- Inflationary Erosion: If you are locked into a 10% interest rate but inflation rises to 12%, the “real” purchasing power of your money is shrinking.

- Gating and Redemptions: In extreme market stress, an investment vehicle might implement a gating fund strategy to restrict withdrawals, though this is more common in mutual funds holding TFCs than in the certificates themselves.

Who It May Be Suitable For

TFCs are typically best suited for specific financial profiles:

- Income-Oriented Investors: This includes retirees or those who want a tangible check in their account to help manage recurring bills.

- Diversifiers: If your portfolio is heavily weighted in equities, adding a term finance certificate provides a different type of exposure.

- Disciplined Savers: Because money is generally tied up for several years, TFCs are a good fit for people with specific future goals, such as a child’s education.

Who Should Be Cautious or Avoid It

Conversely, TFCs may be a poor choice for certain individuals:

- The “Emergency Fund” Saver: You should never put money into a TFC that you might need for an unexpected expense. The difficulty of selling quickly makes it ill-suited for emergency cash.

- Speculators: If you are looking for explosive 50% gains in a year, the debt market will likely disappoint you.

- Risk-Averse Individuals: Those who cannot afford any loss of principal should stick to government-guaranteed instruments.

Alternatives or Related Options

If the structure of a TFC doesn’t feel quite right, there are several other paths to consider:

- Government Securities: These are essentially TFCs issued by the government. While the returns are usually lower, the risk of default is virtually zero.

- Fixed Deposit Receipts (FDRs): Offered by banks, these are simpler to understand and often easier to liquidate, though they rarely offer the higher interest rates of TFCs.

- Income Mutual Funds: Instead of buying one TFC, you can buy into a fund that owns many. This spreads your risk across various sectors.

- Equities: For those seeking higher growth, stocks like PayPal stock offer ownership in a company, though they carry much higher volatility than debt certificates.

Frequently Asked Questions

1. Is my principal amount guaranteed in a TFC?

No. Unlike some bank deposits that are insured, a TFC is only as good as the company that issues it. If the company fails, your principal is at risk.

2. How do I actually receive my interest payments?

Most payments are made electronically. The company or its “paying agent” will deposit the coupon amount directly into your linked bank account on the scheduled dates.

3. What is the difference between a TFC and a Sukuk?

A TFC is a conventional debt instrument that pays interest. A Sukuk is an Islamic financial certificate that complies with Shariah law by providing a share of the profit from an underlying asset instead of interest.

4. Can the company change the interest rate halfway through?

Only if it is a “floating rate” TFC. In that case, the rate changes based on a pre-agreed benchmark. Fixed-rate TFCs maintain the same interest for the duration.

Conclusion

Term Finance Certificates represent a sophisticated and essential segment of the modern financial world. By allowing corporations to borrow directly from the public, they create a pathway for industrial development while offering a disciplined alternative to the volatility of the stock market. While the prospect of higher returns is appealing, it must always be weighed against the reality of corporate risk and market liquidity. A well-informed investor views a TFC as a calculated commitment—one that requires a careful eye on credit ratings and economic trends.