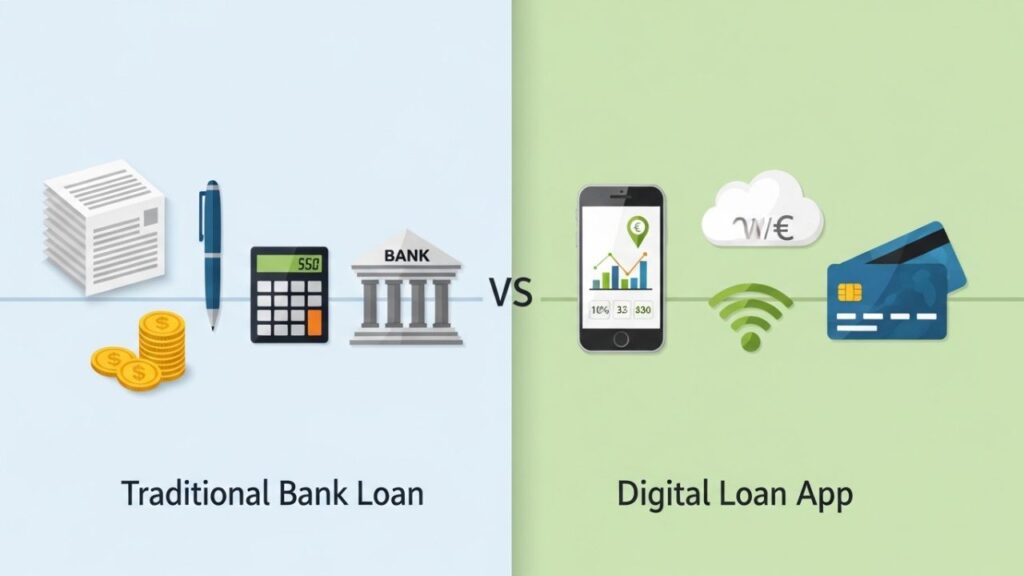

Navigating the world of debt often feels like a balancing act between high-interest rates and the logistical headache of tracking multiple payments. While most people are familiar with traditional bank loans, a significant amount of lending happens “off the books”—between friends, family members, or small business partners. Without a formal system, these arrangements often lead to misunderstandings or missed deadlines.

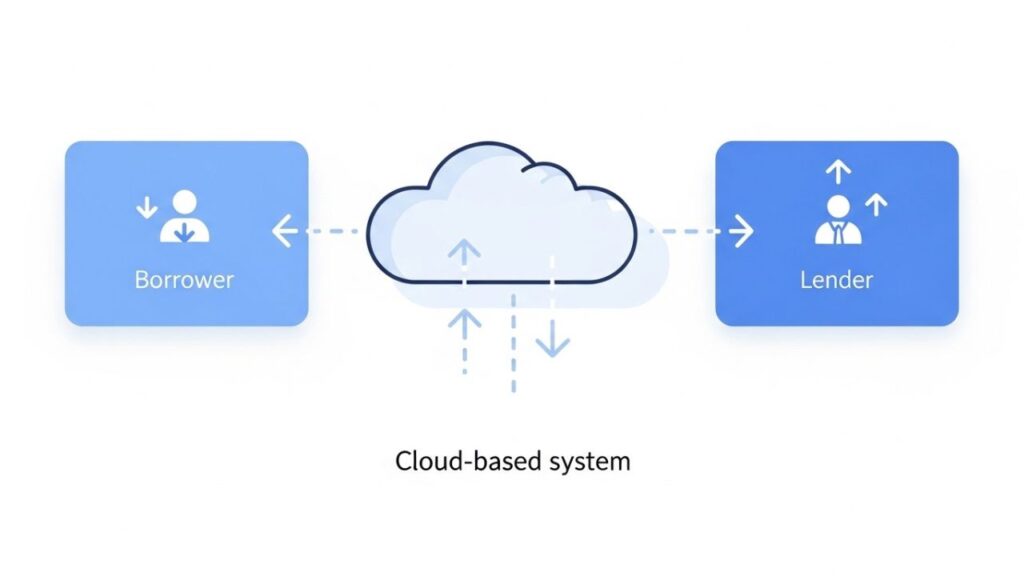

TraceLoans.com enters this space not as a bank, but as a digital facilitator. It is designed to modernize the way we handle informal debt by providing a structured platform for tracking and managing loan agreements. By moving these private contracts from spreadsheets and text messages into a centralized dashboard, the platform aims to provide clarity and professional oversight to everyday financial commitments.

What Is TraceLoans.com?

At its core, TraceLoans.com is a specialized financial technology (FinTech) tool built for loan administration. It is crucial to understand that the platform does not function as a direct lender. If you are searching for a debt consolidation loan—a new lump sum of cash used to pay off various creditors—TraceLoans.com is not the service that provides those funds.

Instead, it acts as a neutral third-party record-keeper. Its primary purpose is to help borrowers and lenders document the life cycle of a loan. Whether it is a personal loan between relatives or a salary saving scheme arrangement, the platform ensures that interest calculations, payment histories, and remaining balances are transparent and agreed upon by both parties.

How It Works

The platform operates by creating a synchronized “ledger” that both the lender and borrower can access. Here is the typical process for setting up a management plan:

- Registration: One party creates an account and undergoes a standard verification process to secure the financial data.

- Defining Terms: The user enters the specific details of the debt, including the principal amount, interest rate, and the repayment frequency.

- Mutual Verification: An invitation is sent to the second party. For the tracking to be official, both the borrower and lender must review and digitally “sign off” on the terms.

- Automated Monitoring: As time passes, the system automatically calculates accrued interest. When a payment is made, the user logs it, and the total balance updates in real-time.

- Communications: The platform handles the “socially awkward” side of lending by sending automated reminders for upcoming due dates.

Key Features or Core Components

The utility of a platform like TraceLoans.com lies in its ability to automate tasks that are usually prone to human error:

- Dynamic Amortization: The system generates a full schedule showing how much of each payment is applied to the principal versus the interest.

- Centralized Documentation: It stores loan agreements and receipts in one secure location, creating a permanent digital audit trail.

- Specialized Tracking: For specific academic needs, the platform can be adjusted to handle student loans tracking for private educational agreements.

- Reporting Tools: Users can generate statements or year-end reports, which are invaluable for personal accounting or tax preparation.

Benefits or Advantages

For those managing private or informal debt, using a dedicated service offers several practical perks:

- Preserving Relationships: By letting a neutral algorithm handle the math and reminders, personal relationships remain separate from financial obligations.

- Accuracy: Manual spreadsheets are easily broken by a wrong formula. A dedicated platform ensures that interest is calculated correctly every single day.

- Accountability: Borrowers are often more diligent about repayment when they see an official “balance remaining” on a professional dashboard.

- Niche Compliance: It can even accommodate specific religious or cultural requirements, such as a Heter Iska loan agreement.

Risks, Drawbacks, or Limitations

Despite its organizational benefits, there are several caveats users must keep in mind:

- No Fresh Capital: This is not a source of funding. If you need a loan to pay off your credit cards today, you must bring your own lender to the platform.

- Data Integrity: The system is only as good as the information provided. If a borrower pays in cash and the lender forgets to log it, the record will be incorrect.

- Cybersecurity Risks: Storing financial contracts online always carries an inherent risk. Users should investigate the platform’s encryption standards.

- Subscription Costs: While basic features might be free, more robust tracking usually requires a fee. Users must decide if the convenience justifies the expense.

Who It May Be Suitable For

- Family Lenders: Parents lending a “down payment” to children who want to ensure the loan is treated with professional seriousness.

- Small Business Partners: Founders who have injected personal capital into a business and want a transparent way to see repayment progress.

- Users of Niche Systems: Those who need to manage specific payment portals like PayMyDoctor.com alongside their personal debt tracking.

Who Should Be Cautious or Avoid It

This platform may not be the right choice for everyone:

- The Debt-Distressed: If you are currently overwhelmed by high-interest credit cards, you likely need a debt relief specialist or a traditional bank.

- The Tech-Averse: Individuals who prefer physical receipts and paper ledgers may find the digital interface more cumbersome than helpful.

- Users Seeking Credit Growth: Since these are private loans, they typically do not help you build a credit score, which is a major drawback for those trying to improve their financial standing.

Alternatives or Related Options

If TraceLoans.com doesn’t fit your specific needs, consider these alternatives:

- Traditional Unsecured Loans: Companies like SoFi or Upgrade provide actual money for debt consolidation.

- DIY Management: Using software like Microsoft Excel or Google Sheets allows for total customization at no cost.

- Legal/Notary Services: For very large private loans (like a mortgage between family members), hiring a legal professional to draft a deed of trust is often safer.

Frequently Asked Questions

1. Is TraceLoans.com a bank?

No, it is a software platform. It provides the tools to manage a loan, but it does not hold money or issue loans directly to consumers.

2. Can I use this for my mortgage?

Traditional mortgages are already managed by professional servicers. This platform is best suited for “private” mortgages or personal loans that lack a bank-provided portal.

3. Does it report to the credit bureaus?

Most private loan management tools do not report your payment history to Experian or Equifax. If you want to build credit, you should look for a lender that explicitly offers credit reporting services.

4. What happens if the lender and borrower disagree on the balance?

The platform relies on “mutual consent.” If a discrepancy occurs, both parties generally need to communicate and reach an agreement before the record can be updated.

Conclusion

TraceLoans.com functions as a digital clerk for the modern borrower and lender. It excels at bringing order to the often-chaotic world of private lending by automating calculations and maintaining a clear history of transactions. However, it is fundamentally an organizational tool rather than a financial product. Before signing up, users should determine whether they need a way to manage an existing debt or a way to fund a new one.